MoneyGuidePro Financial Planning Software Review, Evaluation, and Comparisons |

| Return to the Main Financial Planning Software Review Page | Real cash flow-based Financial Planning Software and Goalware | Current Financial Software Review Status Page |

| Site Information (is listed below. The financial planning software modules for sale are on the right-side column) Confused? It Makes More Sense if You Start at the Home Page How to Buy Investment Software New Financial Planner Starter Kit Professional Investment Portfolio Building Kit Financial Planning Software Support Financial Planner Software Updates Site Information, Ordering Security, Privacy, FAQs Questions about Personal Finance Software? Call (707) 996-9664 or Send E-mail to support@toolsformoney.com Free Downloads and Money Tools Free Sample Comprehensive Financial Plans Free Money Software Downloads, Tutorials, Primers, Freebies, Investing Tips, and Other Resources List of Free Financial Planning Software Demos Selected Links to Other Relevant Money Websites

|

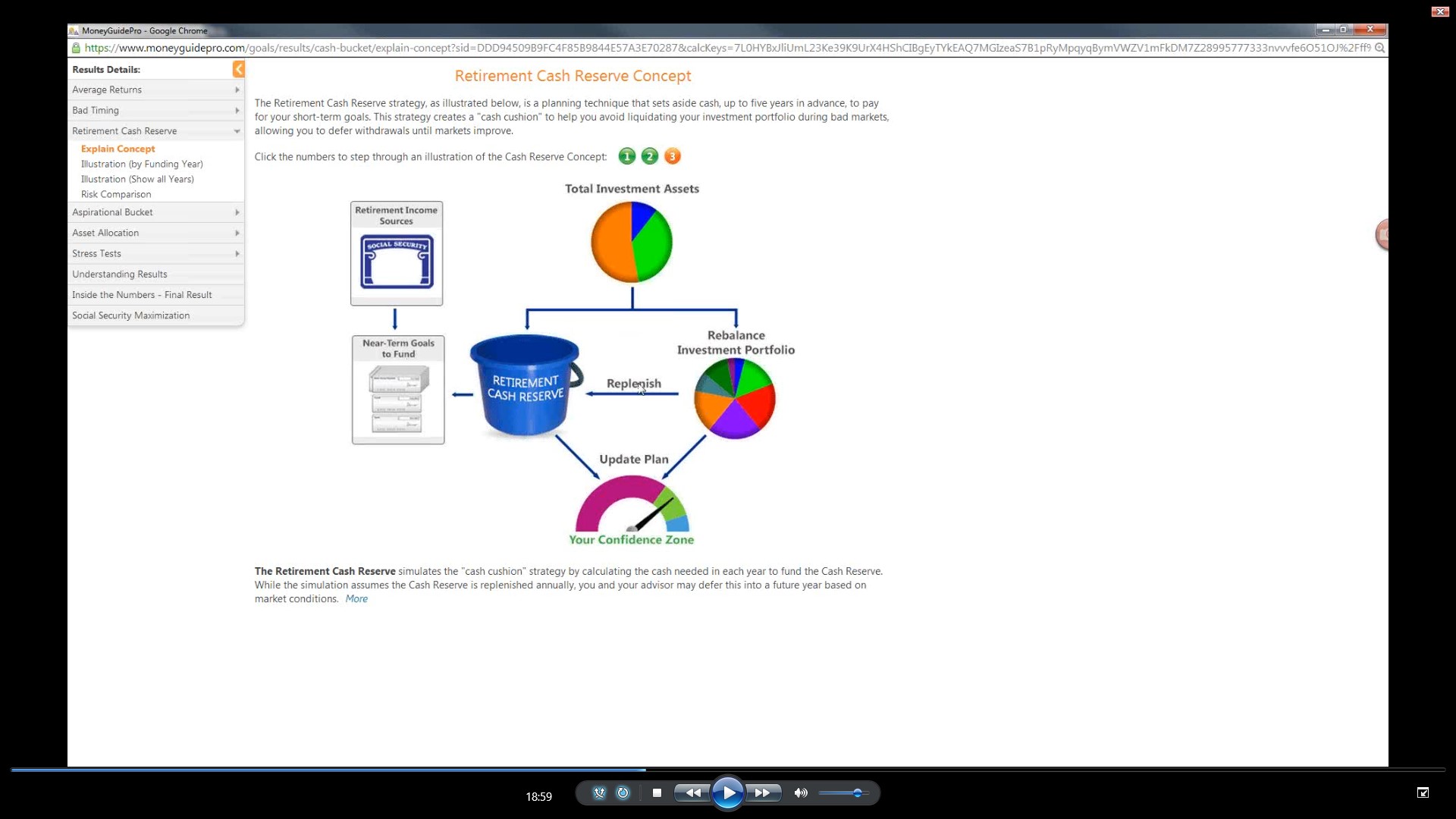

An Overall Product Classification, Generic Review, Evaluation of Their Functions, and Detailed Comparisons with Tools For Money (see the chart at the bottom) We're trying to do a fair and balanced review, so if you dispute any of this, just send an e-mail and we'll look at it and if you're right, then we'll edit that and give you a freebie to thank you MoneyGuidePro Review, Evaluation, and Comparison Generic Description: Sales and marketing tools for Broker Dealer Reps. Market: BD Reps selling life insurance company products. Review Date: June '16. Other Names or Sites They Go By: PIEtech and MGP. What Module on Tools For Money it Competes With, and is the Best to Compare To: Goals-Only Financial Planner. Platform: Code-driven in the clouds, but they don't say what language. Not ISO / IEC 27001:2005 cloud security certified. Read why you should not be working in the clouds when it comes to financial planning software. Read why Excel-based financial plan software is superior to code-driven software. Price: $1,200 to over $2,000 if you tack on all of their bells and whistles. For $1,000 you can buy everything on this site, which provides much more value than just financial planning software. Annual Update Prices: 100%, so you pay full price every year. Tools For Money is only 50%. Finra Reviewed: No, because it has a Monte Carlo simulator. But because MGP is an integral part of The Great Wall Street Cabal, Finra looks the other way and makes a special exception. Monte Carlo Simulator: Yes. Buying Caveats: None found (other than it being cloud-based, and this text from their reports: "MoneyGuidePro results may vary with each use and over time."). Printing: Typical code-based platform where you click print, and it spits out pre-programmed reports in PDF format that cannot be altered by the user (unless you have a PDF editor). With all Tools For Money software, you have total control over all printing. Delivery Methods: 100% cloud-based, so all that's delivered are passwords. With all Tools For Money software, programs are e-mailed after ordering (after that, you'll never have to go online or need an Internet connection for anything). Number of Computers the Program Will Run On: Only one advisor and one assistant can use it, unless you buy their multiple-user deal for much more money. With all Tools For Money software, you can also use anything for anything on an unlimited numbers of computers. Integration and/or Online Downloading: The best integration with other programs and ability to download custodian investment data. MoneyGuidePro Comparison Conclusions, Comments, Opinions, and Observations We've changed our business model to, "If you can't beat them, join them." So instead of whining about MGP, and the damage it's doing to the investing public, we made goalware too). Read about the differences between actual real cash flow-based financial planning software, and goalware. Our past failure on this review page was comparing apples and oranges. MoneyGuidePro is not financial planning software. It is a sales tool for Broker Dealer Reps lying, cheating, and cutting every corner possible in order to get out of doing the actual hard work clients erroneously think they're performing, as they pretend to be financial planners; desperately trying to meet their BD's sales quotas by peddling commission-based American Funds and scaring investors into buying life insurance company products (e.g., annuities). This means it has zero value for do-it-yourself investors (because lying to and cheating yourself with bogus numbers past the first year only has negative value). Fee-only advisers: Your clients are paying you fees so that you'll give them financial plans with valid numbers. You're not using sales tools to dupe investors into generating commissions to meet your Broker Dealer's sales quotas. Therefore, since MoneyGuidePro is incapable of producing valid numbers, either in pre-retirement goalware mode, or in post-retirement mode, it makes zero sense to buy and use it. Goals-oriented planners also have little-to-no value to investors after their long term goals, e.g., retirement, have been met. After retirement, MGP stops goal-focused fantasyland mode, goes into a mode similar to the way our RWR's work. So other than their numbers being inaccurate everywhere, most all goalware isn't blatantly fake after retirement begins. The point here is that when retirement begins, then our simple Real World Retirement planners provide much more value, for only $100 to $250. In addition to the most accurate numbers in the industry, there's a very long list of reasons, features, and functionality that makes MGP's after-retirement programming look like a total joke, compared to our RWRs. The same "modes" apply to the investment module. When working with this module, you're not in the goalware world anymore either. Goalware only applies to generic financial planning before retirement. Here the GOFP works similar to MGP. If the current portfolio is all cash, then you can select one of our existing Model Portfolios. If not, then just use the Comprehensive Asset Allocation Software. Again, and as usual, the list of limitation with MGP's investment modules is just as long as the list of cool features in our investment software. It's a totally different world comparing what you can model with ours compared MGP. The bottom line here is that MoneyGuidePro excels greatly in pre-retirement goalware. But once you're out of that module and mode, their financial software is not competitive, especially compared to ours. It just doesn't perform many functions of value, and costs ten times as much as ours, which performs most all functions users want. In addition to their goalware being fake, the more time goes by, the more confusing and hard it is to use too. Why? Because they're trying everything possible to reconcile fake with actual. Trying to match fantasy with reality doesn't work, and cannot be done, so if you're watching their training videos, and you have no idea what they're talking about, or why this feature even there in the first place, then this is why. They basically didn't do it right the first time, and refuse to change (actually it's not possible to change, because it's not possible to code actual real cash flow-based financial planning software in the clouds, because it's much too complex). So over time, all of these crutches need to be built to stop advisers from whining about it being mostly useless for anything other than being a selling tool. For example, their Retirement Cash Reserve Concept. This is what happens when MGP tries to integrate fake with real. They're trying to deal with the massive errors and omissions that the pre-retirement goalware causes, when forced to shotgun wed the non-fake retirement phase. This is where fantasyland meets reality. When these two different world's collide, it's just a huge train wreck that cannot be fixed. It can't be done, so the result is convoluted kludges that don't work, make no sense, and is not what happens in the Real World. I'm the most experiences user possible when it comes to this stuff, and I still have no clue why this is even in their program. If it makes no sense to me, then no user or client will understand it ether. The only thing I can think of, is that it's a work-around to solve the problem of planners whining about it's lack of functionality. So they just winged it and made something that limps along enough to stop the whining. What advisers need to know, is that the failure here is not the lack of functionality, it's the fact that they're doing everything wrong in the first place. The more the adviser knows about how all of this stuff actually works, the more they're going to find out that The Emperor has no clothes. The error was buying it just because your Broker Dealer made you. Mixing fake with real just doesn't work. Their Retirement Cash Reserve Concept is just another example of what happens when they just do it anyway. So the bottom line here is that the more they try to be not-fake, the more they try to make confusing features and modes to deflect attention away from the inescapable fact that they're just not doing anything right. So it just turns into a mess so huge, that it would be less time, work, and grief than just biting the bullet and using real financial planning software in the first place. Know that everything of value MoneyGuidePro can do (other than deals made with other vendors for integration, ability to see more than two scenarios at once, and the mostly useless estate planning module) can be done better, with minimal fakeness and maximum reality, control, and flexibility; using our IFP. Note that the moving confidence meters weren't listed, because that's all fake, so they have little-to-no value. The IFP also displays all of this information all the time by default. In other words, you don't have to go through all of that confusing input that makes little-to-no sense in reality, to see things like Retirement Cash Reserve, Aspirational Bucket, Allocation Plan, Lifetime Income Plan, or Financial Goal Plan. You just go to those presentation sheets, and what you want to know is just there automatically. That's just what actual financial planning software does. Then, since the IFP is in Excel, you can also use Excel's built-in Goal-Seek function to perform an endless list of What-Ifs that MGP will never come close to being able to do. So other than things that depends on integration, to get data and useless portfolio statistics (from Morningstar, like beta, standard deviation, Sharpe, etc.), then there isn't anything you won't be able to do, that MGP can do, if you have both the IFP and the GOFP. Also, their Client Portal is not a unique feature, because if an adviser wants to let the client play with the plan, then can just e-mail them the program with their input. Then the client has access to all inputs, not just a few, and they don't have to go online, login, and/or have their personal financial information exposed to the world for hackers to exploit.

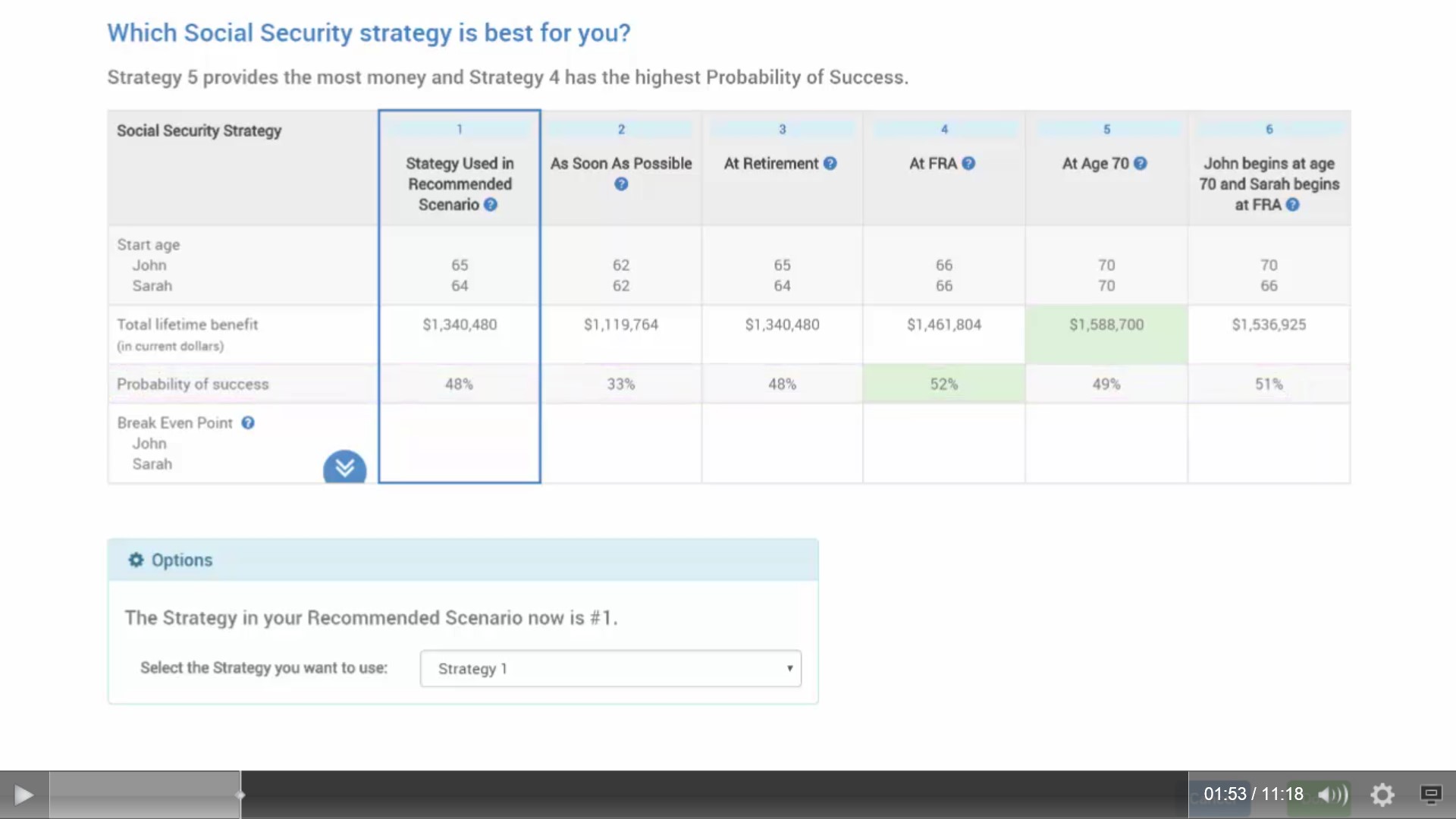

They say in their disclaimers, "All results use simplifying assumptions that do not completely or accurately reflect your specific circumstances." This is a true statement. Goalware simplifies everything to the point that none of it has anything to do with reality whatsoever. So these two types of planware are not comparable. The upcoming GOFP is what will compete with MGP in the goalware space. Look for demos, free trials, and being able to use it around mid-June '16. The table of feature comparisons below still has value while the "MGP Exterminator" is being developed. Then their whole Social Security module is stupid, wrong, bogus, deceptive, insidious, and is a big of a fat lie as it gets. When making a real financial plan, using real financial planning software, and fresh numbers directly from Social Security, all you need to do is run two of the exact same scenarios. In one, input getting Social Security at 70, and in the other, input 62. The plan using 62 will be better every time. It only looks better with MGP (and other goalware) because that's what goalware is programmed to. It's programmed to lie with bogus numbers because that's how BD Reps sell more life insurance company products. It's just as simple as that to understand. That's the truth. Everything else is just a lie designed to sell you something that's bad for you. As you can see below in the Probability of Success row, which are the results of the fakest Monte Carlo simulator in the business, MGP shows waiting as long as you can to collect Social Security retirement benefits is best. So this is just a bold faced lie, because it doesn't even take basic things like the time value of money, inflation, or the risks into account. Remember that goalware does not take anything of value into account, which is why it's fake. Right click to download it so you can see it better.

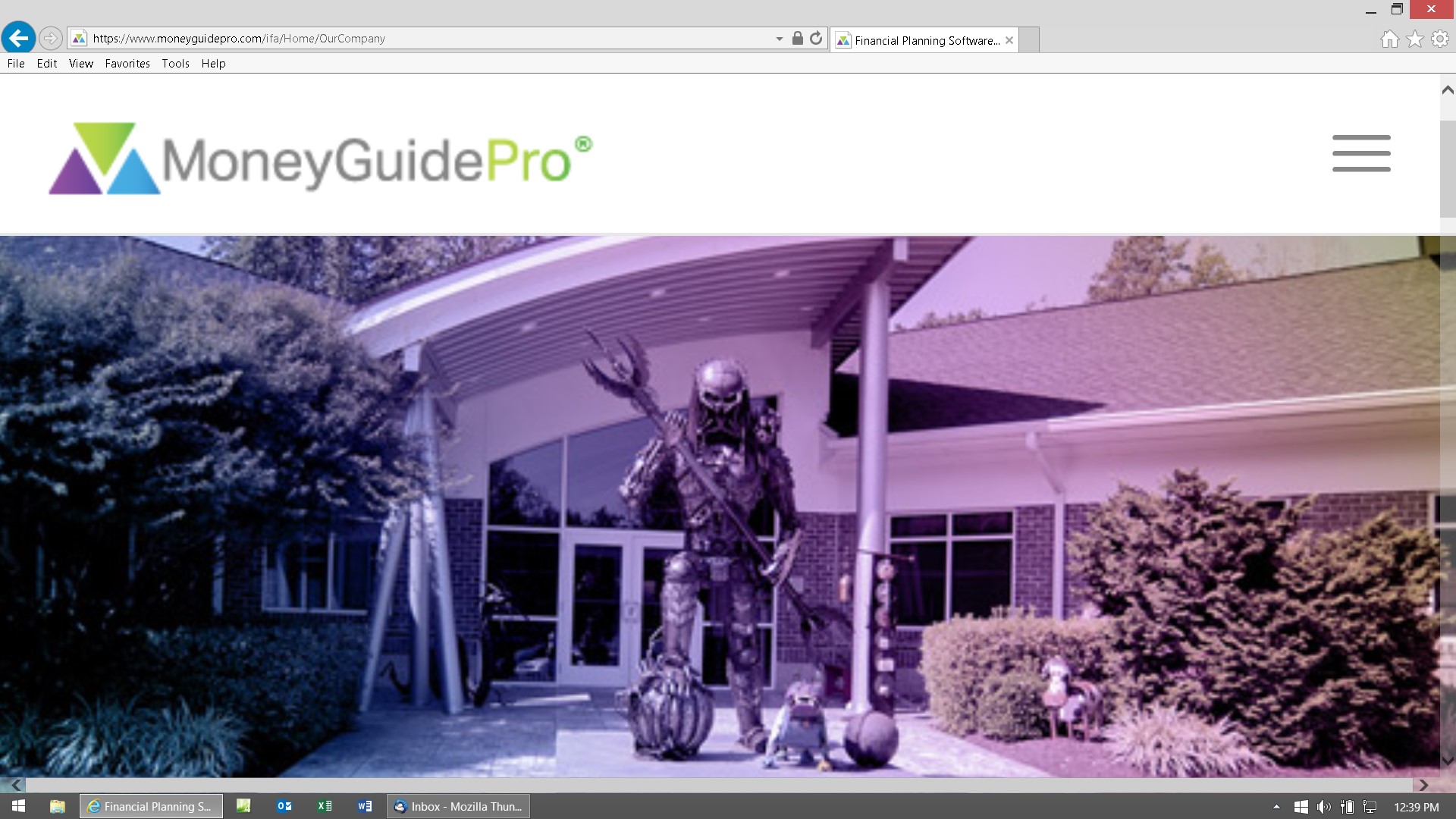

Reports are in PDF, so you can't do anything with them. You can use fancy PDF editing software, but that's so many times the work as using Excel that it's a joke (them saying that it's easy, simple, and fast). It's easy, simple, and fast to print reports, but there's little-too-no beef and then you can't do anything with them. So you can only manipulate reports to look well printed by reinventing the printing wheel (so you're better off just using Excel directly so you can skip all of those steps needed to reinvent the wheel). It's just beyond belief that everyone keeps letting them get away with these shenanigans year after year! Like the old saying goes, "Evil only wins when good is silent." The truth is on this site, so read it until you get it, then say and do something good for a change. Quit failing and start producing quality financial plans. MGP is not even low-quality financial planning software, because it's not even financial planning software at all. It's just a bunch of BS designed to help sell life insurance company products. So their saying, "Everyone deserves a high quality financial plan", is also just not believable. It's totally believable that an evil-doing Wall Street corporation can run amok, lie to everyone, and wreak havoc on the world for decades, and nobody even notices. What's not believable is how y'all just sit there baffled with a blank stare and do nothing about it. Actually, that's totally believable too, because you can't do anything about this Wall Street cabal, so you have no choice but to baaaaaa and be a sheeple and go along with it. Y'all, and investors, not getting that; and not making the appropriate fuss, is what's not believable. Y'all whine profusely about little things that don't matter, like mutual fund management fees; but the big stuff that's actually ruining lives (including your own), y'all are totally oblivious to. That's what's not believable. So I call MGP a Species-level Failure that can't be fixed. Like the comedian says, You can't fix stupid!" So all we can do is get with the black hat program that y'all just can't get enough of, and make better, cheaper, and less fake goalware. The picture below from their website showing their corporate office should be an obvious tip-off to their evil-doing business model. It's the Alien Predator here on Earth preying upon the sheeple (you, the BD Rep). This wasn't an accident, they spent big money putting that there for a reason. The reason is they want everyone to know who they really are and what they actually do. What y'all don't get, is that YOU are their prey. Every time you give them money, it's like them succeeding on their safari, and taking your scalp as a trophy (or since you're a sheeple, more like your fleece). They think they're superior beings (compared to you) out on safari here on Earth, collecting easy scalps of the sheeple. It's just as simple as that to understand their business model: Fleecing of the sheeple for fun and profit. In the movies, the Predators only hunt humans that are also evil-doing predators. They leave the innocent alone (AKA fee-only RIAs and clients with functioning brains). So they're only preying on those humans that are out hunting the weak of their own species for fun and profit - which is the BD business model in a nutshell. They couldn't care less that all they do is wreak havoc and ruin lives. All they care about is that you voluntarily give up your fleece, and then your clients' mutton; just so they can have your scalp as a trophy - which is what you do every time you feed the beast with your money. What a hoot! An evil-doing Wall Street corporation not even bothering to hide their actual business model, "Yup, we're as black-hat as it gets, and our prey has no clue what we're doing to them. All perfectly legal too. Isn't America Great! Show me the money; I mean your scalp, fleece and mutton!"

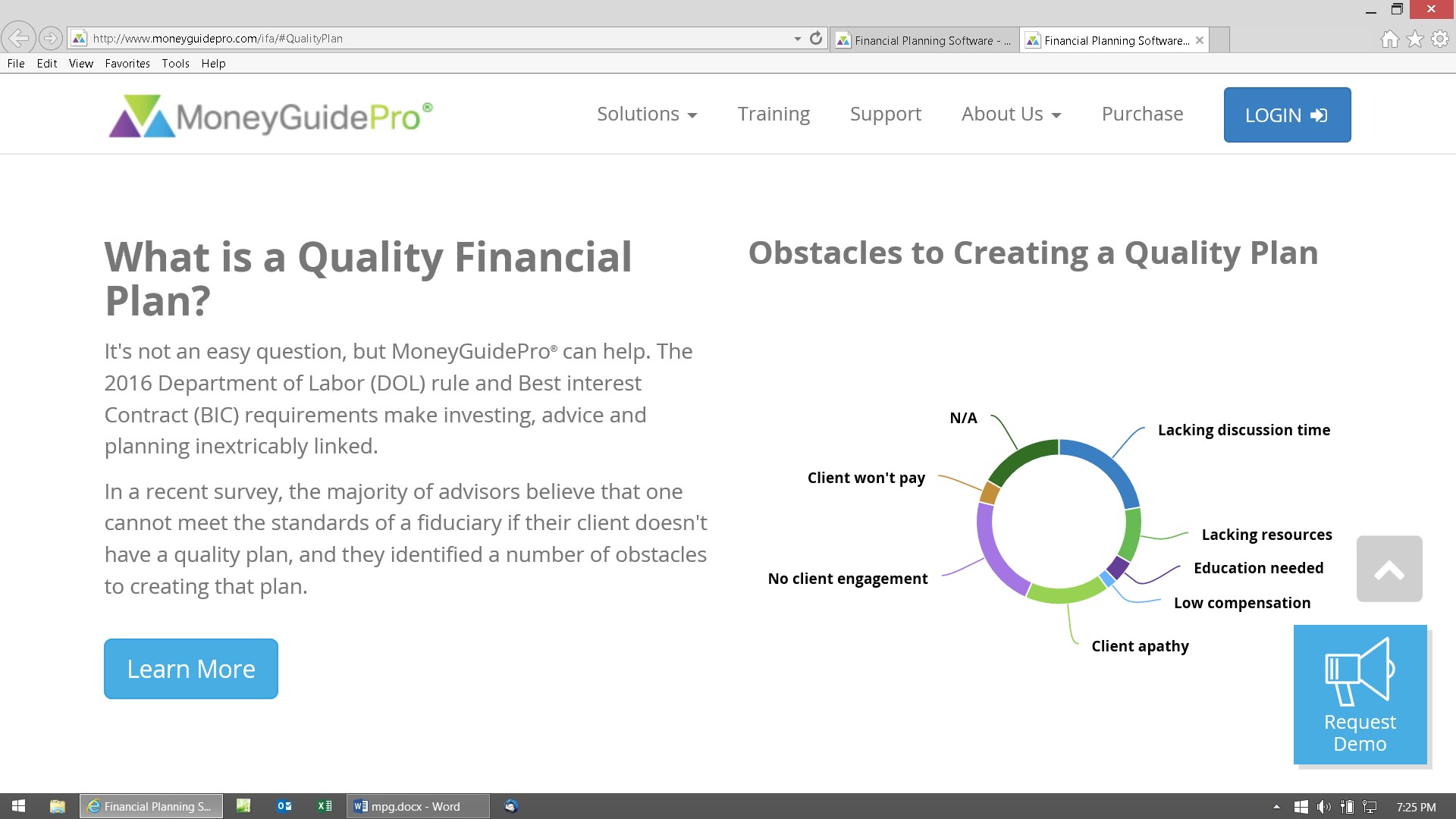

The image below shows an example of MoneyGuidePro's deceptive business practices. What they're doing here is pretending their software is not fake, and then trying to get you to believe that the US Department of Labor "approves" of MGP's "quality financial planware." Just a few minor issues with this top-level deception: First, in order to create a financial plan, one must use actual financial planning software. This means one has to either use our IFP, or NaviPlan, because MGP is the leader in goalware, and thus is incapable of producing an actual financial plan - even a "low-quality" plan. Next, a quality financial plan can't be created unless the user accounts for all of the mundane details that are needed to create a real financial plan. Little minor details like inputting budget and cash flow incomes and expenses, accounting for annual surpluses and deficits and replacement costs, performing an actual investment risk tolerance test instead of having someone move a meaningless slider, and an endless of critical Real World variables that MGP just completely ignores. Next, they may be surprised that the government is not is as oblivious, nor as easy to get to rubber-stamp approval of Wall Street shenanigans, as they have been in the past. What they're doing here is thinking that, and hoping that, the government remains oblivious to reality, and just keeps believing that MGP is actually financial plan software. This time may be different. The government may have grown enough brain cells to finally get it on this round of at least attempting to actually do something to fix all of these massive failures. In which case, someone with the required attention span will eventually get around to calling shenanigans, and banning goals-based software completely. All one needs to do is read the image below, figure out how MGP actually works, and then it should be obvious that the two things are diametrically opposed to each other - and thus the text in the image is just a big fat lie that needs to go the way of the dinosaurs. MGP is the kind of software that is THE epitome of what the government needs to ban, if they want advisers to start acting like fiduciaries, instead of used car salesmen. So MGP is trying every dirty trick in the book to deflect attention away from the fact that DOL is out to change the color of advisers' hat from black to white. MGP is the #1 "enabler" in the industry that allows advisers to keep their hats as black as possible. In other words, if MGP was banned, more than half of unsuitable investment recommendations (if you want to call life insurance company products investments, which is laughable), would magically vanish overnight. So they have a team of high-paid marketing lobbyists pulling out all the stops to ensure these deceptions continue to wreak havoc on investors for all time. And they're the best in the industry too. You probably have read this and thought, "Okay, so MGP is working with the DOL to ensure it makes quality financial plans that meet the new fiduciary standards. What's unusual about that?" HA!!! If so, then that's an example of how good they are at pulling the wool over your eyes. If they can deceive you, then also deceiving the failed government just happens by default. They're not doing anything to work with anyone. All they care about is that the new DOL Fiduciary Rules won't affect them at all. That's the main goal they're trying to accomplish. And they'll probably succeed too. In this case, they're just pointing to a sign that says, "Nothing to see here, move along," and hoping that the DOL reads it and thinks, "I don't know squat about financial plans, let alone the difference between a low-quality and a high-quality financial plan. C'mon, I'm just a government employee with zero financial skills, education, and experience! MGP is bold enough to put a big thing on their website boasting that their software makes quality financial plans. I guess it must be true, so I'll just move along and look for something else to whine about elsewhere." They think the government is so stupid, that they'll just read the sign and move on. They may be right, as this is what always happens when they try to stop Wall Street shenanigans. Wall street just outthinks, outguns, and outspends them, and thus gets whatever they want, most every time. Critiquing their text: No MGP cannot help, it can only hurt. There's not one thing that MGP does that a true fiduciary would approve of. What's the source of this "recent survey?" C'mon, it's MGP, there's no survey. They just made it up, it's just a fake falsehood deception, just like everything else they do. Then they left out by far the #1 obstacle to "creating a financial plan" in the Real World in their pie chart. Creating an actual financial plan is hard work, and advisers (especially BD Reps) just do not perform any kind of hard work anymore, period. Since the beginning of time, they've just gotten used to the fact that any and all deceptions can be used to move life insurance company products, using minimum work and maximum shenanigans, regardless how Black Hat they are; and everyone thinks it's just fine. Well, those days are slowly coming to an end, with the new DOL Fiduciary rules being hopefully the first step. That's THE problem in the industry since '05 or so. If there's any actual work / time / thinking / attention span / skills or education required, or reality involved, or any "knowing what you're doing;" then the average financial adviser will just say no. Why? Because they don't have to. Why work when you don't have to? Nobody is forcing them to perform actual work. Nobody has in the past, nobody is now, and more than likely, nobody will ever force financial planners to actually be financial planners in the future. These days financial advisers are too dumb, broke and broken, sleep-deprived, confused, lazy, technically challenged, and incompetent with near-zero attention spans, to create a financial plan - even a non-quality financial plan. BD Reps demand goalware that will allow them to make commissions while performing the bare minimum of work, while making it look like they actually did some work to clients. This is what MGP specializes in - the great "Quality Financial Plan Deception." Nobody does it better, and it's just the end result of letting all of these massive government failures fester since the beginning of time. All of this is just as simple and easy to understand as that.

|

Financial Planning Software Modules For Sale (are listed below) Financial Planning Software that's Fully-Integrated Use the IFP for $2 a day Goals-Only "Financial Planning Software" Retirement Planning Software Menu: Something for Everyone Comprehensive Asset Allocation Software Model Portfolio Allocations with Historical Returns Monthly-updated ETF and Mutual Fund Picks DIY Investment Portfolio Benchmarking Program Financial Planning Fact Finders for Financial Planners Gathering Data from Clients Investment Policy Statement Software (IPS) Life Insurance Calculator (AKA Capital Needs Analysis Software) Bond Calculators for Duration, Convexity, YTM, Accretion, and Amortization Investment Software for Comparing the 27 Most Popular Methods of Investing Rental Real Estate Investing Software Net Worth Calculator (Balance Sheet Maker) and 75-year Net Worth Projector Financial Seminar Covering Retirement Planning and Investment Management Sales Tools for Financial Adviser Marketing Personal Budget Software and 75-year Cash Flow Projector TVM Financial Tools and Financial Calculators Our Unique Financial Services Buy or Sell a Financial Planning Practice Miscellaneous Pages of Interest Primer Tutorial to Learn the Basics of Financial Planning Software About the Department of Labor's New Fiduciary Rules Using Asset Allocation to Manage Money Download Brokerage Data into Spreadsheets How to Integrate Financial Planning Software Modules to Share Data CRM and Portfolio Management Software About Efficient Frontier Portfolio Optimizers Calculating Your Investment Risk Tolerance |

| Financial Planner Features and Functions | GOFP: $12 (1/100th of MGP) | MoneyGuidePro: $1,250 to over $2,000 |

| Annual Update Prices | $12 | 100% of what you initially paid |

| Lifetime Subscriptions Available | Yes | No |

| Do You Have to Buy it for a Whole Year? | No, you can pay a whole $2 to use it for one week | Yes, you have to pay their whole annual cost to use it, even if you only need it for a week |

| Are You Spending Hundreds of Dollars Per Year in Software Licensing Fees to Feed a Small Army of Travelling Software Salespeople to Fly Around the World Schmoozing Advisers into Buying their Software (with lavish fine dining, gifts, freebies, and entertainment)? (If it says, "Yes" to the right, then their budgets for that are in the millions a year. YOU are paying for that, and it provides zero value to you in software features - all it does is add hundreds of dollars to their prices) | No | Yes |

| Asset Allocator Module | Yes | Barely, very primitive with little control over anything important |

| Number of Asset Classes their Asset Allocation Software Uses | Unlimited | 11 (ten plus one miscellaneous, so only one can be changed). It "doesn't do much of anything" so you'll still need to come up with your own investment Strategy and funding options yourself |

| Deals with Pre-retirement Annual Cash Flow Surpluses and Deficits (the very heart of the financial plan) | No, it's "goals-orientated" | No, it's "goals-focused" |

| Integration with Other Financial Software and/or Ability to Download Account Holdings from Online Custodians | Yes to both | Yes, it has the best integration with other programs |

| Gets Detailed Annual Expenses, Incomes, and Income Goals at Retirement from other Software (like our Personal Budget & Cash Flow Projector) | No, it's not "cash flow-based" so most all critical details are ignored | No, it's not "cash flow-based" so most all critical details are ignored |

| Built-in Budgeting and Cash Flow Modules | No | No |

| Accounts for Budgeting of Replacement Costs | No, totally ignored | No, totally ignored |

| Built-in College Planner Module | Somewhat, little better than using a free online college calculator | Somewhat, little better than using a free online college calculator |

| Life Insurance Calculator Module Included | Yes | Yes, a very primitive capital needs calculator that's little better than using a free online life insurance calculator |

| Ability to Project Life Insurance Needs into the Future | No | No |

| Life Insurance Needs Module: Ability to Account for Replacing ALL Incomes, Set the Number of Years for it to be Replaced, the Percentage of it to be Replaced, then have a Unique Discount Rate Input for All Incomes Individually. Next, Ability to Choose Between Inputting Needs and Available Resources via Manual Input or Automatically (where numbers are internally generated from inside the financial plan) | No to All | No to All |

| Life Insurance Needs Module: Ability to have the Same Features and Functionality for Calculating the Client's Capital Needs if the Spouse Passes in Every Year | Yes | No |

| Ability to Easily Stop Life Insurance Policies (paying for premiums and face values), and/or Change Face Amounts (or premiums) in Any Year | Yes | No, once you input a life policy, everything runs amok forever, even after retirement |

| Number of Versions | Unlimited | Unlimited |

| Ability to Easily Make a Proposed Plan from Current Plan Data | Yes | No |

| Ability to See ALL Inputted Data on One Page | Yes | No |

| Total Control Over Printing | Yes | No control at all, unless you want to edit PDFs (you'll need special hard-to-use software to do that) |

| Ability to Perform Any and All Advanced "What-if" and Scenario Functions | Yes | No to very limited, Super Solve only lets you have about five scenarios |

| Built-in Portfolio Optimizer | No | Yes, but fake, like everything else |

| Monte Carlo Simulator | Yes | No, only iterates rate of return, then it uses standard deviations, which is "wrong." Says it iterates over 1,000 times, but that's a lie, unless you read their fine print, then they say it's less than 100 |

| Monte Carlo Simulator on the College Planning Modules | No | No |

| Ability to Designate a Financial Plan as the Current or Proposed Version with One Click | Yes, there all the time, no need to click | Yes, there all the time, no need to click |

| Ability to See Both Current or Proposed Versions at the Same Time | Yes | Yes |

| Input Spouse's Data Separately | Yes | Yes |

| Designate an Asset Account as Belonging to Client or Spouse | Yes | Yes |

| Designate an Asset Account as Jointly Owned | Yes | Yes |

| Ability to Have Client and Spouse Retire in Different Years | Yes | Yes |

| Total Control Over Social Security Between the Two People Separately | Yes | No |

| Ability to Change Social Security Income for Each Person Separately, AND in Every Year | Yes | No |

| Ability to Control the Social Security Tax Inclusion Rate in Every Year | Yes, you can choose between 0%, 50%, or 85% in each year | No |

| Ability to Set the Age Social Security Starts for Both People Separately | Yes | Yes |

| Ability to Include Any and All Sources of Annual Miscellaneous Expenses, in Addition to the Generic Annual Income Goal | Yes, you can control every dollar in every year | Yes, but limited |

| Ability to Include Any and All Sources of Annual Miscellaneous Incomes | Yes | Yes, but limited |

| Ability to Control Withdrawals Using IRS Age 70½ Required Minimum Distributions | Yes | Somewhat |

| Ability to Control Withdrawals Using IRS 72t Distributions | Yes, all three methods | Somewhat |

| Investment Account Payout Methods | 9 | 1 (maybe more, but couldn't find how to input them) |

| Ability to Change Asset Payout Methods Midstream | No | No |

| Ability to Start and Stop Asset Withdrawals at Any Year | Yes | No |

| Ability to Start Asset Withdrawals After Retirement Has Begun | Yes | No |

| Ability to Start a New Asset at Any Year (even after retirement has started for anyone) | Yes | No |

| Ability to Set Asset Account Rate of Returns to be Whatever You Want in Any Year | Yes | No |

| Ability to Have Total Control Over How Much Asset Account Contributions are, and When They Start and Stop Annually | Yes | No, you can input contributions but there's little control over much |

| Ability to Control the Tax Rate in Every Year | Yes | No |

| Ability to Set a Tax Inclusion Rate on Each Asset Separately | Yes | Somewhat, limited |

| Presentation Page (report) that Shows Each Non-asset and Asset's Estimated Withdrawal Taxes in Every Year | Yes | No |

| Ability to Simulate Roth IRAs and Conversions | Yes | No |

| How Many Years the "Window" Is | 75 | No window at all, then it seems to stop at 40 years |

| Both Client and Spouse Can Have their Own Separate Income Goals, and they can be Whatever You Want in Every Year | Yes | No |

| Ability to See and Print All Miscellaneous Incomes and Expenses in Every Year | Yes | Somewhat |

| Displays the Present Value of Additional Capital Needed to Fund the Combined Income Goal Deficits in Every Year | Yes | No |

| Displays All Basic and Advanced Pertinent Retirement Planning Information | Yes, much more relevant data displays than any other retirement planner | Very limited |

| Calculates and Displays How Much More Money is Needed to Reach the Retirement Goal as Monthly Payments Until Retirement | Yes | No(?) |

| Calculates and Displays How Much More Money is Needed to Reach the Retirement Goal as a Current Lump Sum | Yes | Yes |

| Calculates and Displays How Much More Money is Needed to Reach the Retirement Goal as a Current Lump Sum in All Years | Yes | No |

| Allows You to Set a Unique Rate of Return on How Much More Money is Needed to Reach the Retirement Goal (AKA discount rate) | Yes | No |

| List All Assets with Pertinent Data (e.g., asset values, percentage this asset is of the whole, age when it becomes effective, contributions, payout ages, payout methods, rate of return assumed, and amount of income subject to taxes) | Yes | Somewhat, but limited |

| Lists All Non-Asset Incomes with Annual Amounts, Ages When They Start, COLA Inflation rates, and if it's Taxable or Not | Yes | Somewhat, limited |

| Everything Everywhere Displays Year, Both Ages, and Year Numbers for Quick and Better Understanding | Yes | No |

| Ability to Account for Fixed Assets Like Defined Benefit Pension Plans and Annuitized Annuities | Yes | Yes |

| Control Over Pensions Between the Two People Separately | Yes | Yes |

| Ability to Set a Survivor's Pension to Pay Out Reduced Benefit After Death | Yes, with total control over annual amounts too | Yes |

| Ability to Set an Annual COLA Rate for Fixed Assets Like Defined Benefit Pension Plans and Annuitized Annuities | Yes | Yes |

| Ability to Have Pensions and Other Assets Pay a Death Benefit to Cash Flow | Yes, with total control over annual amounts too | Yes, but there's little-to-no cash flow accounting going on in the first place because it's not "cash flow-based" |

| Displays the Amount of Annual Deficits When You'll Probably Run Out of Money | Yes | No |

| Displays When You'll Probably Run Out of Money (AKA "Gap funding") | Yes | Yes |

| Displays Annual Percent of Annual Income Goal Being Met | Yes | No |

| Displays Balance of Available Capital in Every Year With Percentage Increase or Decrease from the Previous Year | Yes | No |

| Displays the Average Weighted Rate of Return on All Investment Assets Combined in Every Year | Yes | No, unless you (input and) use a pre-defined model, then limited |

| Displays the Present Value of Additional Capital Needed at Retirement in Every Year | Yes | No |

| Displays the Present Value of Additional Capital Needed at Retirement in the Current Year | Yes | No |

| Number of Informative Charts and Graphs You can See While Working Already Set Up | Over 800 | Only one or two per "screen" |

| Ability to Make as Many New Charts and Graphs as You Want | Yes | No |

| Ability to Change Charts and Graphs Any Way You Like | Yes | No |

| Detailed Chart of All Annual Miscellaneous Incomes and Expenses | Yes | Somewhat, limited |

| Ability to Control Income Goal Inflation Rates Both Automatically and Also Set Them to be Whatever You Want in Every Year | Yes | No |

| Layers of Annual Inflation of Income Goals | 5 | 1 |

| Ability to Set the Ending Year so Numbers will Stop Showing to Reduce Clutter | Yes | No need as there's usually no window at all showing annual numbers |

| Displays Each Person's Life Expectancy Age Using IRS Unisex Mortality Tables | Yes | No, uses an ancient and erroneous mortality table |

| Ability to Set a Life Expectancy Age Independently of the Calculated IRS Life Expectancy Age Using IRA Unisex Tables | Yes | Yes (they call it "Planning Age"), but uses an obsolete mortality table |

| Displays the Difference in Years Between the Inputted Life Expectancy Age and the Calculated IRS Life Expectancy Age | Yes | No |

| Displays Both the Number of Years and the Percentage of Retirement Years Where There's Both Sufficient and Insufficient Capital | Yes | No |

| Displays the Total Current Value of Assets and Total Current Annual Contributions | Yes | Somewhat, assets are usually all lumped together into one of their pre-defined models, so you have little-to-no idea what's actually going on with them |

| Displays All Sources of Income and Tells Where They're Coming from in Every Year | Yes | Somewhat |

| Ability to Set the Number of Trailing Zeros on Presentation Pages (so it won't show values down to the dollar if you don't want to see that much detail) | Yes | No |

| Input Validation and Detailed Error Messages to Tell You what You Did Wrong and How to Fix it | Yes | Yes(?) |

| Accounts for Any and All Types of Investment Assets, Including Rental Real Estate | Yes | Somewhat, limited |

| Displays Detailed About How Much Retirement Income is Being Withdrawn from Each Asset Individually | Yes | No |

| Has "Flexible Assets" that Pay Out Retirement Income Like Life Does in the Real World (AKA "as needed") | Yes | Yes, that's its main payout method, so little control over much if you want to model anything else |

| Allows Inputting of Investment Assets Using the "Bucket Approach" (used by asset allocators and retirement planners that want to model scenarios like depleting non-qualified assets before tapping into qualified assets) | Yes | No |

| Ability to Calculate Detailed Needs for Both Disability and Long Term Care Insurance | Yes | No, very little calculations done because it's not cash flow-based |

| Asset Account Draw-Down Analysis Tools | Very Limited | Comprehensive |

| Deals with Technical Details of 401(k)'s - like Catch-Up and Matches | Yes, you can integrate the IFP with the Most Functional 401(k) calculator | No |

| Ability to Turn Assets Providing Retirement Incomes On and Off Individually | Yes | No |

| Displays How Much in Investment Assets are Needed to Fund Annual Income Goals After All Sources of Non-asset Incomes are Accounted For | Yes | No |

| Displays Different Colors to Designate Between Client, Spouse, Both, and Data that Does Change With Input, and Not | Yes | No |

| Comes With a Detailed Fact Finders for Gathering Data From Clients | Yes, comprehensive | Yes, but not great |

| Comes With a Free Effective / Average Tax Bracket Calculator to Help Determine Inputted Tax Rates | Yes | No |

| Displays All Years of Information Automatically | Yes | No, little-to-no window at all |

| Complete User's Manual with Detailed Directions on How to Do Everything | Yes, including a list of Real World options if you run out of money too early, and much more valuable retirement planning information) | No, very limited help screens are only available when you're at the section of the program. They put all of these resources into having a computerized voice read you the same too-limited text |

| Phone and/or E-mail Support | Yes, but for more money, but it's rarely needed because there's little-to-no bugs and the directions are more than sufficient - few people e-mail or call for support anymore these days | Yes, included |

| Platform | Excel Based (making it extremely stable, inexpensive because uber-expensive code programmers don't need to be employed, bug free, will always work on any computer (Mac or PC) with Excel, any and all operating systems, and rarely needs of any kind of updating) | 100% cloud-based |

| Transparency | Total, all data flows logically from left to right as if you were reading, then you can use Excel or a hand calculator to verify all numbers so you easily can trace EVERYTHING back to your input. No secrets, no surprises, no mysteries, just awesome data | None |

| Ability to Save Individual Client Files as a Unique File Name (so you can back them up onto your physical computer, so you can access old client input data even years after you let the software expire) | Yes, it's just a spreadsheet, so you have total control over saving client files. Not only that, you'll always have your client input data even when programs expire. Then you can just copy and paste it into the new version if you Update, or use it to input into other programs | Yes, but they stay in the dangerous cloud, so you can't back them up on your computer |

| Tax Software Included (software that will calculate taxes due, like TurboTax, or in reality, just estimate the current year's taxes due) | No | Not really, it doesn't even look like they tried to perform this futile task |

| Cost Benefit Ratio Feature | Yes, unique to the IFP | No |

| Number of Computers One "Copy" Will Run On | Unlimited, just spreadsheets you can use on any computer with Excel 2007 or later installed | Two at a time unless you pay more for the multiple user license |

| Modular Too | No, it's an integrated goalware program. Get the individual modules that are not fake if that's what you want | No, it's just one big program, so you'll need to buy and input more than what's Needed if you want to run a quick simple modular report |

| Ability to "Go Back in Time" (to input a plan, to see how things worked out in the current or a past year) | No | Yes |

| Accuracy of Numbers | Best of all goalware, but still fake | The worst of all goalware products, nowhere close to reality |

| Dangerous Installation Procedure that May Wipe Out Windows (DLL) Files if They Screw Up (making a reload of Windows needed, which is more work than having to buy a whole new computer. Yes this kind of thing happens all the time with code - e.g., ExecPlan's free demo in '08) | No | No, cloud-based |

© Copyright 1997 - 2018 Tools For Money, All Rights Reserved