About Monte Carlo Financial Planning Software |

| Fully-Integrated Financial Planning Software with Monte Carlo | Retirement Planning Software with Monte Carlo Simulators | College Savings Calculator with Monte Carlo Simulations |

| Site Information (is listed below. The financial planning software modules for sale are on the right-side column) Confused? It Makes More Sense if You Start at the Home Page How to Buy Investment Software Lifetime and 5- to 15-year Extended Subscriptions New Financial Planner Starter Kit Professional Investment Portfolio Building Kit Financial Planning Software Support Financial Planner Software Updates Site Information, Ordering Security, Privacy, FAQs Questions about Personal Finance Software? Call (707) 996-9664 or Send E-mail to support@toolsformoney.com Free Downloads and Money Tools Free Sample Comprehensive Financial Plans Free Money Software Downloads, Tutorials, Primers, Freebies, Investing Tips, and Other Resources List of Free Financial Planning Software Demos Selected Links to Other Relevant Money Websites

|

What Monte Carlo software is good for, what it's not good for, and why you've been hearing so much about It

Monte Carlo simulations are also known as stochastic modeling, stress testing, and worst-to-best case scenario analysis We're not a fan of Monte Carlo simulators in financial planning software. But customers kept asking for it, so we implemented it into the Integrated Financial Planner, all versions of our retirement software, and the college planners. They utilize a unique, more robust and realistic methodology of performing Monte Carlo simulations, compared to other financial planning software vendors. Why we're not a fan is explained below, along with how and why some of these shortcomings are negated by the way our financial planning software is programmed. Most retirement planning software uses Monte Carlo simulators to randomly fiddle with the rate of return on the inputted investment accounts, to give you a bottom-line probability of success number. Our simulator also fiddles with cost of living inflation, and the global tax rate, in addition to asset rates of return.

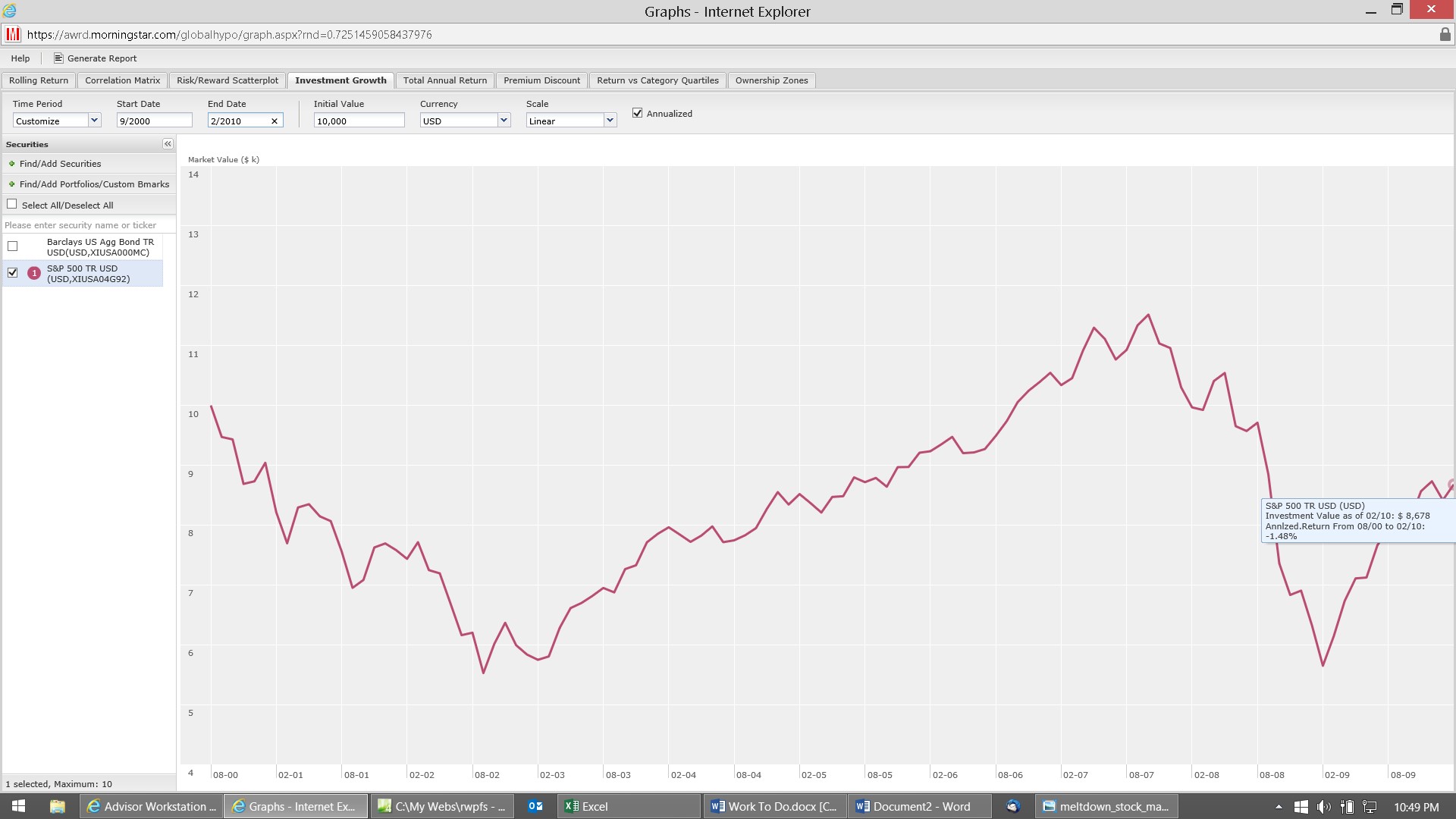

What Monte Carlo Actually Is Monte Carlo is a city in Monaco that's famous for gambling, more specifically, roulette wheels. The ball rolls around and it lands on a number on the spinning wheel at random. If it lands on your number, which has a probability of one in 38, then you win. That's how this type of software got its name - inputs to its calculation engine are iterated at random. For retirement software, usually the only input iterated is the investment rate of return. That's about it, so mystery solved. The first Monte Carlo simulators were used when designing the first atomic bombs at Los Alamos Labs, NM, in the 1940's. They needed to simulate thousands of different random outcomes of the detonation, so they used random inputs into a complex computer algorithm as a way of doing this. It worked very well. Why? Because everything to do with that followed the laws of nature and physics, thus math calculus produced valid results. Mathematician Stan Ulam coined the name in 1946, refering to the casino in Monaco where his uncle borrowed from family to gamble. According to math site, Motherboard.com, "Mr. Ulam was inspired to develop the method with his partner John Von Neumann while playing solitaire and trying to calculate the likelihood of winning based on the initial layout of the cards." Then Monte Carlo simulators were eventually adapted for business applications, mostly by Hertz, in 1964. Monte Carlo simulators (sometimes) use random input numbers to form complex financial models for assessing various types of risk (the probability of a bad financial outcome - which is usually losing money). But in the context of personal financial plan software, Monte Carlo refers to the randomness of rate of return input data. You've just started to hear about it in the 21st century, because computers have just recently become powerful enough to perform these CPU-intensive tasks. A simulation on a 20th century 486 or single-processor Pentium computer would take days to calculate all of the outcomes, and then another day to plot the probabilities from these outcomes. Since it's practical to market now because of fast computers, what you have is Monte Carlo being added to everything to make more money selling financial software. Then the usual self-reinforcing academic articles came to let people know these programs are on the market (how to buy now). So a new mini-academic-fad was born. What you need to do is realize what Monte Carlo is, what it's good for, and what it's not good for. Just because it sounds cool, spends a lot of time computing, is being heavily advertised, and used by other fields of finance, doesn't mean it will do anything of value for you or your financial planning and/or investment management clients. Like the old saying goes, "Just because you can do a thing doesn't mean you should, nor do you have to do that thing." It's basically a gimmick used to raise a vendor's flat or falling financial planning software sales. You're hearing about it because it's relatively new, and there's no other news to report in the world of boring retirement planning software. It works okay for use in modeling portfolio losses and unexpected losses, when pricing options and other complex derivative security strategies. Why? Because you can use math calculus on them. Options and futures are contracts, where if the price of this does this, then this happens. The only randomness is the price of the underlying security. So they vary that one-dimensional input, and then the simulator can produce valid results. This validity does not extend to retirement plans, where there's too many random variables to count, in addition to the main iterated rate of return input. That's the point. Retirement plans are much too complex for the pathetic simulators we have today to deal with. Next, it's important to note that there must be a "goal" in the simulation. If there's no goal, then there's nothing to simulate. So when financial plan software vendors say their software simulates anything before retirement, then you either misunderstood, they're misleading you, or there is a cash flow savings goal somewhere it's trying to solve for. In other words, you can't run Monte Carlo on anything pre-retirement, because retirement is the main goal. The only other goals it can solve for are things like college planning. So if you're thinking a vendor "has Monte Carlo before retirement," then you're either wrong, they are wrong, or the goal is something like a college plan (or saving for another type of long-term financial goal). Here's another example of where Monte Carlo simulators produce valid results in the world of money: Say a stock analyst wants to forecast earnings for a corporation. They will input many criteria into the modeling software program, and then give it a target EPS (earnings per share) number - say $1.00 per share (that's the goal it's solving for). The simulator will then come up with an EPS number based on every input that's iterated. Since there can be dozens of inputs to get the EPS number, and all of these inputs can vary within a range of what's reasonably expected to happen, it would take a person an eternity to input all of these variations within the range of possibilities into a financial calculator, or spreadsheet. Now computers can do this work automatically in seconds. It just runs one iteration with one set of inputs. Then it varies that by one increment and runs it again. Then it stops when all iterations within the set ranges are complete. Then it reports the percentage of iterations that either failed or succeeded. If enough output data are available, then probability distribution charts can be plotted. So let's say this stock analyst is using real Monte Carlo software, and wants to calculate the probabilities of EPS being at least $1.00. If one run (one input iteration based on one set of Free Cash Flow data, say $900,000) comes up with $0.99 of EPS, then that would be a false outcome, because it needs to be at least $1.00 to be a true outcome. This one iteration would create one statistical data point with a 0% probability. Now let's say that the next FCF input is set to $1,100,000 and another run is made. EPS is computed to be $1.01, and a true outcome is logged. Adding these two iterations together, the probability is now 50% of realizing EPS of $1.00. Instead of incrementing FCF up a notch each iteration, and re-running the simulation, each iteration may be input as a number selected at random, within a set range by the user. This is all Monte Carlo does. The program allows the user to set iterations and ranges for each input. Some just use random numbers within a specified range, and there are so many iterations that essentially all variables within that range are simulated (and duplicated many times too) Or sometimes inputs and ranges are not internally randomly generated, but manually defined by the user. For example, the user may tell it to make 100 iterations on the FCF input field - starting at $950,000 and increasing by $1,000 until it gets to $1,050,000. Here the simulator runs the first iteration at $950,000, and then logs a true or false answer. Then it runs the next one at $951,000, and logs a true or false answer. It does this 100 times up to the last value of $1,050,000. The results create a log of true and false outcomes, and that's all it takes to construct a probability distribution curve. This will then give you a bottom-line answer like, "You have a 73% chance of realizing EPS of $1.00, given these ranges of FCF input parameters." All this means is 73% of the outcomes were true, and 27% were false. Then with a probability distribution curve, one can generate meaningful statistical data, like standard deviations. This is what it is and that's all there is to it. There's no magic, no crystal ball, no arcane mystery. It just saves the user from having to manually input thousands of different combinations of data, by having the simulator do it automatically. This sort of works, because determining an EPS number is found just by adding up other numbers. So the only thing random are the inputs themselves. In other words, there's not much randomness going on when you're just adding up something simple, for example, 2 + 2 - 2 + 2 = EPS. The point is that in retirement planning, each one of those 2's have dozens of associated random variables attached to it. None of which are accounted for by the simulator. So it's not possible for it to produce a valid result. Then everything is repeated in every year, so it's also multi-dimensional. Whereas in the EPS example, you're only working with one dimension, because the time frame is usually one quarter of one-year - so there's no compounding going on at all. So not only do retirement plan simulators fail because of the multi-dimensionalness of having to deal with more than one-year, it also fails because it can't account for the linkage between the years - which is the compounding of money (AKA the "tree-trunk" problem discussed below). True Monte Carlo simulators allow the user to set iterations and ranges for dozens of input variables. When it does this, the computer runs the same simulation millions of times with one combination (not permutations) of input data. This is why it's so slow, and why only newer computers can perform these functions in a reasonable period of time. Most financial plan software vendors with Monte Carlo use it in their retirement planning modules. The most-common usage is to see if the fund of money will last until some assumed age (usually life expectancy), given an assumed rate of return on investment accounts. It just runs numerous iterations with various random investment rates of return. This then gives you a bottom-line probability based on all of the true and false outcomes. The main problem is that it doesn't let the user set the number of iterations, nor the range of assumed values. It just makes all of this up for you based on what the vendor wants (which Most always has little-to-nothing to do with what may happen in the Real World). Another problem is when it's married to a database of historical benchmark index returns and/or standard deviations, which allows the user to select a prior time frame's rolling return or sigma data. When you can go way back in time like this, to a period so foreign to our current reality that it's like being on another planet, this increases the resulting probability number by 10% to 40% over what will probably happen in the future. So you're telling people their plan has X% probability of success, when in reality, it's up to less than half as much. This is because if you let it use stock market return data going back to 1926, then it's going to be using rates of return that are twice as high as you'll actually see these days. So if you do that, then it will be iterating average annual rates of around 9% to 12%, when you know the probable band of 10-year average rolling returns nowadays have been permanently lowered to around 5% to 8%. Another problem, is using historical rates of return like this is assuming that 100% of the investment portfolios are in the benchmark used, most commonly, the S&P 500. So when you tell it simulate using the S&P 500's returns, then it's going to assume those long-term historical rates of returns (and/or standard deviations) - on all of the client's asset accounts. The point is that nobody in their right mind would put all of the money they have into 100% equities like that. There's always a healthy dose of bonds, cash, international, real estate, etc. This reality is not accounted for in any Monte Carlo simulator by any vendor. I have yet to see one where you can set the past benchmark to use more than one asset class at the same time. Just adding that additional dimension would require it to take all day to calculate. So just that failure alone makes their results bogus, and vastly overestimates the resulting probability number far into fantasyland. This is also why our results show numbers that are usually less than half of other vendors. This is because we're assuming reasonable long-term rates of return on a normal, sane, rational, well-diversified investment portfolio. We're assuming someone will hold a portfolio allocation that a sane investor would hold in the Real world - including accounting for holding almost 50% in bonds during retirement. Other vendors assume you're going to hold 100% in the S&P 500, and then average around 9.5% over a thirty-year time horizon. That's just not going to happen. Nobody has averaged more than 8.5% on a normal, sane, rational, well-diversified investment portfolio over any twenty-year rolling period in the history of ever, nor will they ever. So this is an example of a Monte Carlo simulator being allowed to run amok like a wild animal, just like an unconstrained portfolio optimizer. You think you're doing the "right thing" for people by using the very longest averages possible, but it turns out this is what's moving your retirement plan from reality into fantasyland. This is not serving anyone's best interests. Just the opposite - you're setting people up for a major life failure, because if they plan on that, then they will not realize these rosy rates of returns, and then they will run out of money before passing. When a very simple sample financial plan was input into the IFP, and the same data input into NaviPlan in 2012 - the IFP's Monte Carlo number was 23% and NaviPlan's was 31%. So let's say their number is 5% too high just because of using dangerously optimistic returns, then 4% of the difference is from not iterating inflation, 3% from not iterating taxes, and then the rest is just from the combination of all of these rosy scenarios and omissions compounding upon each other. That's why NaviPlan's bottom line Monte Carlo probability numbers are so rosy sky high. It tells people their chances of retirement plan success are usually more than twice as high as they really are. Then this is NaviPlan, the "industry leader" with the "best calculation engine." When you get to the MoneyWhatevers (MoneyGuidePro, MoneyTree, eMoney Advisor, etc.), they don't even care, nor even attempt to be accurate in any way, as most everything about their plan software is just "fake." This makes it all virtually useless, because you're relying on a probability number based on only one factor (the average rate of return on investments) in only one dimension. In order to properly use Monte Carlo in retirement planning, dozens to hundreds of inputs need to change to reach a Real World probability number: Life expectancy, age of retirement, investment payouts, yields vs. share selling, investment returns, inflation, income goals, Social Security, all of the types of taxes, pension payouts, annual cash flow surpluses and deficits, random earned incomes, replacing vehicles every ten years, allocation mix changes over time; and then duplicate all of that for every investment individually, then for the spouse, then account for all of that compounding in every year, and the list goes on and on. Because of those dozens of other dimensions that are not accounted for, it's just so far from reality that there's not enough words in the dictionary to type with. No personal financial planning program on the market today is true Monte Carlo because none give the user the ability to control these input ranges and/or set the number of iterations for even the few most critical input fields. It only iterates one. This is because vendors feel advisers don't have the required brain power and/or attention span to perform this kind of tedious work, they won't spend that much money on a true multidimensional simulator, and they won't wait hours for the results to compile. Advisors don't have that kind of time to spend on generating retirement plans - they whine now when the IFP takes half an hour to simulate. This is the bottom-line everyone should keep in mind - it's not near as cool as one is being led to believe, because its application is limited to only one variable, global asset rate of return, when it should be applied to dozens, if not hundreds. Our financial plan software is more robust, and paints a more realistic picture, because it iterates two more of these critical variables at once (taxes and inflation). Also, when Monte Carlo is used in asset allocation (or anything having to do with predicting investment returns), the proper name for it is "portfolio optimization." So if you're reading that a new asset allocation / investment program has Monte Carlo, it's really just someone incorrectly slapping the Monte Carlo name onto a portfolio optimizer just to increase sales. They think you'll buy it, just because you don't know any better. Why We're Not a Fan of Monte Carlo Simulators This page is whining about Monte Carlo simulators, because: • Monte Carlo simulators, and/or software, does not do anything to overcome or account for financial market volatility, nor does it reduce risks of any kind. It will not help you when it comes to losing money you've invested. It will also not help you retire earlier, predict the future better; nor will it help keep you from outliving your retirement investments. What will it do that is actually useful to your life - not much of anything! • It's also the program function that makes Finra not give financial planning software approval letters to BDs. Finra rightly tries to ban its usage on a case-by-case basis whenever it can. Why? Because it's mostly a "bogus" number and feature, it should be banned for the good of the investing public. • No financial plan software vendor has a Monte Carlo simulator that performs this function properly, nor paints a realistic picture of what will probably happen in the future. • The above problem will never be solved by any vendor. • If the simulation takes less than an hour on a newer computer (e.g., a PC with an i7 CPU, or on a powerful cloud-based server), then it's just not possible that it can be doing anything useful, valid, or meaningful. Any simulation that takes a few minutes is a complete facade. • Financial advisers have been brainwashed by financial plan software vendors into thinking that Monte Carlo is one of the needed and/or required magic Holy Grails of financial software; and without it, they'll lose their clients to more on-the-ball advisors that can "wow" them better with fancy charts and graphs. Then this is constantly reinforced by academia and the press, only because they can't think of anything else that's actually useful to "justify their existence;" and because they live in a world of "publish anything today, or die". News flash: Advisers will never lose a client because their financial plan lacks a probability of success number. Never will a client say, "Where's my probability of success number that I so desperately crave?" When it comes to this, they don't understand, don't care, don't believe in it, and won't remember. The only things they really care about are their advisors not "running off to Mexico with their money," being adequately insured, how they're going to pay their current bills and debts and retire someday; and then not losing a significant portion of their money when the markets go down, all while not being gouged by the adviser. That's basically the extent of what goes on in the brain of the average client. If you don't believe that, just ask them, and then you will see. After your brilliant presentation about the Monte Carlo number, ask them if they care. Then you'll get that the only reason they care is if you told them the number has actual validity in the Real World. So just don't do that, and everyone will be much better off (especially you, the money adviser). So the only time clients' have ever heard about Monte Carlo, is when a financial planner presents it to them. Then that's a memory that lasts about a week. If you don't believe that, then ask clients what they remember about your financial plan presentation that's more than a week old. Then you'll get it. If you think that's harsh criticism, then contact any government regulator (at Finra, the SEC, the CFPB, your state finance department, etc.) and they will all tell you the exact same things. This is why Finra won't even review investment software if it has a Monte Carlo simulator built into it. They'll say it's all so far past pie in the sky fantasy, that they want to ban it. When advisers think it's valid and tell people the resulting numbers have actual meaning, when they do not, it makes them want to throw their hands up in the air in despair and scream. The only ones that care about the results of Monte Carlo simulations are advisers; and they should be the ones that get it to the point that they're telling their clients to just ignore it all. Why that's true is next.... • Monte Carlo simulators, and portfolio optimizers, are the only two things in the life of a financial adviser that provide intellectual stimulation. So if you take away the only "fun" part of their "jobs," then their lives become boring, tedious, repetitive, annoying, and mundane. Without it, there's nothing cool to talk about. Hint: Asset draw downs are now the "current fad," so use those draw-down calculators as something to talk about instead. That is not what they signed up for, as young ambitious bright-eyed and bushy-tailed whippersnappers out to set the world on fire with their brilliant financial analytic skills. While in college, they had stars in their eyes and envisioned a perfect world, where everything they were spending their bottom dollar and the prime years of their lives on learning was going to set them up to be rich and famous investment guru "rock stars." Their sound and complete understanding of how the Real World economy works combined with their brilliant market timing skills, would enable their ETF trading to make so much more money than their competitors, that they'd be in the spotlight daily with TV reporters following them around asking what they think the markets will do next because of the daily news; and uber-rich clients would be beating their doors down wanting them to manage all of their money for whatever they wanted to charge them. After graduation, and then a year or two of living in the cold harsh realities of this business, it becomes clear that none of that will ever happen. So they fight tooth and nail to hold on to the one thing (or two things), that attracted them into the business in the first place - which is being a "financial analyst" and being well-paid to think about and figure out complex "Wall Street stuff." Look at it like this: The average financial planner is like Al Bundy, Peter Griffin, or Homer Simpson. Monte Carlo simulators, and portfolio optimizers, are the only "beer" in their lives, that otherwise suck. The slightest hint that someone may even mention going down a road that may lead to taking away any of their beer makes them "very grumpy." That's why, right now, you want to call and/or send an e-mail to grump about this page. You can give up portfolio optimizers and/or Monte Carlo simulators in your practice about as much as you can give up whatever the "beer" is in your personal life. I know because when I got into the biz (which was two decades before Monte Carlo simulators, because computers were way to slow to handle them), I thought I'd be spending most of my time playing with portfolio optimizers, going; "Wow cool look at that! If I did that with my clients' money, then I'd be the best ever and would be rich and famous in no time; fascinating, and yay this is so fun! Boy did I ever get into the right business. This sure beats being a plodding chip engineer in Silicon Valley. Any day now Wall Street is going to call me begging to take their multi-gazillion dollar job in Manhattan, and I'll be the new rich and famous money guru!" WRONG! TOTAL COMPLETE FAIL! If I was born twenty years later, then you'd just replace portfolio optimizers with Monte Carlo simulators (or add to it), and it would have been the exact same failure. Over 95% of my time as a money adviser was spent on cold-calling, prospecting, marketing, preparing to sell product, scheduling and rescheduling trying to get people to come into the office, closing the product sales, doing mountains of monotonous paperwork, keeping up with the prospecti farm and BD compliance, making and printing financial plans that I knew I'd never get paid for (because back then there was no fee-only RIA model), studying to take exams and CE courses, driving all over the place, spending my own money on all of the above, listening to clients During Fact Finding Discovery and pretending to care as they whine about how their opulent lives are not perfect, managing idiot sales managers, and sitting in boring meetings (having to endure endless sales pitches by American Funds wholesalers and other similar moronic time-wasters). So most advisers know the reality compared to the fantasy about two years into building their practice. This is a huge letdown! So they really want and need that "beer" to keep their brains interested. This is such a huge psychological factor, that it's the #1 reason why I gave up being a financial advisor, and decided to be a money software vendor. I need that "daily beer" so badly, that I switched careers, and ended up making much less money over the long-haul. But at least this software stuff keeps my brain interested and busy. So I know exactly why you want to whine about this page, and it's not your fault; it's just another float in the never-ending parade of failures that comprise this whole broken industry. • Because of the above, vendors keep trying to beat new life into this dead horse, which then feeds this feedback loop vicious cycle of naivety, hype, and misinformation. So this page is here mostly to provide information that will help deflate the hype and put the tool in its proper place. If financial advisers didn't think this was the best invention since sliced bread, then there would be no reason to whine. But they do - and they're just wrong. This performs a disservice to their clients, because advisers are telling them whoppers about what Monte Carlo does, when it does not. This "fact vs. fiction error" is the problem. When everyone from vendors to clients understand this is not to be taken seriously, then I'll stop whining. But vendors and advisers seem to make more of a fuss as time goes on. Every year, instead of vendors making their financial plans function properly, their simulators keeping getting more bells and whistles added to them. Then the more this happens, the more green advisors are seduced by them. Then the more this happens, the more they want to whine about this page. It's just as simple as that. What You Should Do About this Situation Don't make a mountain out of a molehill. Because some detail-oriented financial planners like to torture themselves with arcane features of financial plan software, vendors have responded. They've come up with all sorts of ways to make Monte Carlo simulators, and their results, more fascinating, exciting, and useless at the same time. The more complex simulators are, by using data like past standard deviations on a market index, making tornado graphs, making colorful moving speedometer dials, and allowing more control over the return base; the more useless and unrealistic they become. This gives the adviser more to talk about, but it does little-to-nothing of value for anyone in the Real World. In addition to it not working as advertised: • Client's don't get it. • Client's don't believe it. • Client's don't care. • Client's brains freeze up as soon at it's mentioned. • Clients won't remember. • The results are dependent upon assumed input ranges and iterations (which cannot be defined by the user). So you don't know what any of the inputs were that created the result. If you have a very low probability result, then why? What set of inputs did that? There's no way to tell, because it's all locked up in their code. Most simulators will just give you a bottom line probability number, and will not display the actual outcomes of a pessimistic simulation (nor any set of input iterations). So that's another huge limitation, that can only be solved with good old manual input using intelligent realistic ranges. In other words, if you want to see the outcome of an exact pessimistic scenario, you can't do that with most simulators. The only way to do that is to manually input it. • It assumes the generated statistical distributions are normal, when they are not. • It assumes correlation coefficients are zero (or one), when they are not. • Return inputs are not linear. They go up and down at random over the input time frames. • Inflation, asset class returns, taxes, and most everything to do with money (sigma, beta, Jenson, Treynor, Sharpe ratios, etc.) cannot be predicted from historical data. So iterating long-term benchmark standard deviations has no value. These one-dimensional risks are even more random, unstable, irrelevant, and unpredictable than simulating long-term past rates of return on benchmark indices. Whatever caused X% amount of sigma risk and/or volatility in the S&P 500 in 1995 has near zero applicability to it today. It's a totally different world, so it should not be simulated. Then when they are used, they're being applied to all of the client's assets. Which is incorrect, because investors do not hold 100% of their money in any one benchmark. They also hold bonds, cash, and other asset classes. No vendor's simulator allows the user to properly account for any of this. • The user is forced to let the simulator globally iterate the rate of return on every investment account, all in the exact same manner, all at the same time. In other words, when an iteration calls for a 1% rate of return on assets (and/or a 10% standard deviation), then these values apply to all inputted investment assets, regardless of their asset class. This is so, even if there are significant accounts holding nothing but, or mostly, cash, short-term municipal bonds, fixed annuities, or rental real estate. This is another major failure. To fix that, simulators would need controls for each investment asset, so you could tell it to not iterate returns on each account individually. To perform this function properly, the user should also be able to set the range of input values from this to that, on each individual asset individually. No code-based vendor would even contemplate adding the extreme programming complexity stemming from those multiple extra dimensions into their Monte Carlo simulator. Even if their code programmers could, then that would increase wait times far beyond unacceptable ranges. In other words, it would take an extra hour to run the simulation. Then it would add yet another $500 increase in annual costs. But you can easily simulate all of these types of realistic scenarios with all of our financial planning software. • It's just a dull tool to perform blunt stress testing, so the only thing of value is the bottom line probability number - which is wrong and mostly useless (especially if all it does is only iterate the rate of return and/or apply standard deviations to all of the inputted investment asset accounts globally). What should you as an advisor do about this situation? When presenting the retirement plan, just tell them the bottom line "stress test" probability number. If it's more than 75%, then tell them things look good. If it's between 50% and 75%, tell them there's reason to be concerned. If it's below 50%, tell them more resources need to diverted toward reaching the goal, or the goal needs to be dialed down. That's all, because they don't get it, care, believe, nor will they remember most of what you're saying the next day. All they're going to remember more than a day later is if their plan looks good, okay, or bad. The thing they're going to remember most a week later, is the amount of more money their financial plan said they need to invest, and if they should do that or not using that adviser's investment strategy. Not making a mountain out of this molehill will save you work and time presenting it, will not waste the client's time, and will not promise them unrealistic fantasies that can't come true (and may come back later to haunt you). It will also not freeze up their brains, so they'll have more attention span to comprehend what's really important - which is financial plan implementation. So if you're wondering why client's say, "Time out, I need a coffee bathroom smoke break!" right when you're getting down to the most important part of plan presentation, then this is why. So just don't do that, and then their brains won't be tired when you're closing their deals. Then your closing ratio may magically go up, resulting in you probably making more money - all for doing less work in less time. So torturing yourself trying to find financial planning software that has the Monte Carlo simulator that you agree the most with, will take dozens of hours a year in research keeping up with what vendors are doing. Then you're paying for that - up to $500 a year more. It's a never ending parade of Whac-a-mole when it comes to vendors adding the same bells and whistles to their simulators. They're doing this because they think they need to have the shiniest newest iToy to get advisers to have enough attention span to consider buying it. So they're constantly "improving" their simulators. Not because these new bells and whistles actually perform any function of value, but just to keep advisors interested, so they can make more money. Their iToy has to be new, shiny, high-tech, and better than before, or they won't make the sale. So just take a step back to realize what you're doing. You're wasting serious time, work, and money on something that's mostly useless, unrealistic, always wrong (because only ours paints a realistic picture), and has little-to-no relevance in the Real World; all just to pin a stress test number on a goal. Then no matter how hard you try to get people to be as excited about it as you are, they won't be. You'll have to spend quality time explaining it to people in detail so they'll understand. Then you'll have to do it over and over again. Then they'll say they get it, when they don't and just want you to move on to something they care about. If you don't believe this, then just ask them! They'll tell you it's a cool and interesting feature, but they don't believe in it, so they don't care enough to remember. Call the client a week later that seemed to like, care, and understand it the most. Ask them to tell you what they remember about your dissertation during plan presentation. Then you'll see for yourself that you've made a mountain out of a molehill. Basically the more excited you are about this, the more "you just don't get it." The more you know about the technical details about how all of this actually works in the Real World, the more you'll realize it's just a tool to do a job. Then the tool doesn't do the job it's hyped up to do. It's just not possible for Monte Carlo simulators to do anything useful when it comes to personal financial planning or retirement. The sooner you get over it, the better off everyone will be. So don't waste precious resources making a mountain out of this molehill. Use it to do its job, but don't make a fuss about it. It's not worth the resources, mostly because it's "fake" and nobody cares but you (and the software vendor). Okay, so even after all of that, advisers still want to e-mail and call about the technical details of Monte Carlo simulations. So the big question now is: After reading all of this, you should know that it's a facade, bogus, 75% fake pie-in-the-sky bull-puckey. Other than for sales purposes, why are you defending it? It's just a bell or whistle. So it generates an interesting number. But it's not megaphone worthy - just ringing a small bell worthy. If you are a professional financial adviser, and you're spending more than a minute explaining it, then you're failing by wasting their time on something "bogus." You're basically lying to them if you tell them this number has any real meaning, importance, validity, or relevance in the Real World; because it does not. You've just been brainwashed into thinking this is real from someone somewhere - like a NaviPlan training class, academic articles, college class, or your sales manager teaching you how to misuse MoneyGuidePro into making quick and dirty annuity, American Funds, and whole life insurance sales. So if you're an actual professional, then you need to go back to that source and re-learn everything until you get it. If you're an investing consumer, and you're spending more than a minute thinking about this number, then just don't. Bang your head softly on a wall, as that's going to result in the same outcome as trying to understand something that software programmers invented for no better reason than they think it's needed to sell their software. Just like us, they do it because their competitors have it. Does it work, do anything useful, or sell more software? No, but sales may go down if you don't have it. So that's the one and only reason why it's there. Really, that's all there is to it. That's the long version of why Monte Carlo simulators in financial plan software programs are so controversial. The medium version is this: Monte Carlo simulators function and produce useful results in the Real World only when all of the variables function via the laws of physics, nature, and conform to the rigidity of calculus. These variables also have to be all non-random, have normal distributions, quantifiable with agreed-upon standards and units of measurement; and then the basis of the original hypothesis needs to be sane, rational, and logical. All of that is the exact opposite of everything having anything to do with money! That's why it doesn't work. Rewording to fit personal financial planning models: Monte Carlo simulators do not function realistically nor produce useful results in the Real World, because none of the variables function via the laws of physics or nature. There is also no math or calculus in any branch of economics or finance that can predict the future of anything whatsoever. These variables are also all random, have abnormal distributions, are not quantifiable; and few agree upon mundane standards and/or basic units of measurement. Then the basis of the original hypotheses are rarely sane, rational, nor logical. For example, thinking you're going to average more than 8.5% on a diversified portfolio in the 21st century (where bonds yield nothing, giving them no upside with massive downside risks) is not sane nor rational. You may realize that miracle for a number of five-year rolling periods, but you're not going to average that over twenty years - like most simulators will and do. Most simulators are pre-programmed to average around 9.5%, which nobody has ever done in the history of ever, even back in the 20th century, when you look at twenty-year rolling returns. Very few people got close to that even back when bonds yielded much more than nothing after inflation. So the only way to get more than 7% long-term is to load up on stocks. If you do that, then you're going to lose a ton of money when the government does what it does best - which is screw most everything up for most everyone, causing flat to down markets that last for years, if not decades. Then if not our government, then there's plenty of other idiot governments that are capable of starting yet another great debacle fiasco that could crash the stock markets for decades (Russia, China, North Korea, or any Middle Eastern country and/or Baltic / Caucus / Stan-state). Just so you know, if you call or e-mail wanting to debate this, then I'm just going to say debate over, not interested (unless you've recently bought something for $500 or over, or you want to pay $25 for an intelligent answer). If people had new and/or useful information to debate with, then I'd welcome that; but it's the same things over and over. Sorry, but not I'm interested in spending that kind of quality time on this subject anymore. Everything is here already. Empirical Criticism of Monte Carlo by People In-the-Know Download a Wealth Management magazine article about the drawbacks of using Monte Carlo simulators Mark Kriztman, CFA; well-known author in the financial planning and investment management field, found a major flaw in most all vendors using Monte Carlo in their software. He wrote about the fact that at the end of each year, simulators reverted to the base number instead of "continuing from the trunk of the same tree," which is what happens in the Real World via the compounding of interest rates. For example, let's say that you input a 10% base annual rate of return, and then you tell the simulator to use a range of ±20%. Its worst-case iteration is going to be a -10% rate of return (+10% + -20% = -10%). Assume it used this worst case -10% in its last iteration path. In the next iteration, instead of continuing the next compounding period from -10% where it left off, it reverts back to original base trunk rate of +10%. So if the next iteration is +2%, then the correct rate of return applied should be -8%. But it resets itself, using +12% instead. This is not correct, and proves that today's simulators are not capable of working with more than one dimension. It neglects the fact that markets can have more than one-year in a row with huge negative investment returns. In the Real World, you can easily lose 75% more money than the worst case iteration models. This also dramatically understates volatility. Just this flaw alone makes the results meaningless. So the bottom-line is that Monte Carlo usually does not do the main function that it's hyped up to do - which is to create an end result probability number based on all of the best and worst case scenarios. It may compound positive returns fine, but usually ignores the compounding of negative returns. This is also why our simulation results show a much lower probability number than you may be used to seeing. Other vendors paint a rosy scenario because of their many fails. No code-based vendor has yet to overcome this tree-trunk problem, nor allows the user to control or vary the inputs enough to make Monte Carlo worth much, yet. Someday, when computers are 100 times faster, and advisers are willing to pay ten times more for it, then this may happen. Now about why the huge number of iteration runs a program simulates doesn't matter: Let's say, for example, that a Monte Carlo run generates a random simulated ten-year list of investment returns like this: 8% The average annual compound rate of return over this ten-year horizon would be 2.32%. The program used up ten iterations to do this. This could have been done in one iteration of 2.32%. So even if the tree trunk problem was solved, the average over the long haul still can be summarized in just one iteration. So don't be impressed when a vendor claims its Monte Carlo simulator is superior because it can have 10,000+ runs. All this is going to do is make it take an eternity to complete. Over 80% of them are just randomly generated duplicates. This is why generating an enormous array of random numbers is not needed. This is critical in scientific work, but not in financial planning. Then if you read the fine print, no simulator uses the 10,000+ iterations like it says it does. It may say that on the big print, but when you look at the disclaimer, it will say it uses some type of "enhanced methodology," that gets the same results of using 10,000+ iterations, when only using ~500 (e.g., MoneyGuidePro). If it actually used 10,000+, then it would take hours, not minutes, to calculate on the fastest computer. Also don't be impressed when a financial planning software vendor says their Monte Carlo simulator uses historical standard deviations of a benchmark index, other asset, or portfolio, when determining the ranges of returns used. Historical performance (returns, standard deviations, or covariances) has little-to-no predictive ability. The only guarantee in the world of money is what happened in the past will not happen in the future. The long-winded version of why historical performance isn't a good predictor of future performance is on the last section of the portfolio optimization page. The bottom-line is that not one of these portfolio statistics (sigma, beta, Jenson, Treynor, Sharpe, etc.) have any predictive value whatsoever. It's interesting to see what these stats have been in the past on whole portfolios, and/or on individual assets; but none of them have any consistency at all. If they "flop around wildly all the time at random," then they are useless when it comes to making predictions. If they did have any predictive value, even just a little bit, then we'd have been using them over two decades ago. As one should know, all of this "back testing" has little-to-no predictive value because financial assets respond randomly to complex sets of financial variables, which are then traded by irrational emotional humans that have diverse reasons for trading; none of which can be predicted by anyone nor any computer software program. For example, Microsoft could go down 10% in one day, just because Bill Gates decides to sell a bazillion shares to fund his saving the world foundation. Nobody could have predicted that unless they followed him around all day every day and had access to his brain. So the best way to run simulations is to just make a range of most likely outcomes, then iterate down the list in reasonable increments. This eradicates the duplicates, and greatly decreases the wait times. There also is little-to-no difference between 2.32% and 2.3% when it comes to successes or failures in retirement plan software. So rounding things down to one decimal place will also eliminate a significant number of useless random iteration paths that don't do anything but increase wait times. This is what we did. We eliminated most all of the duplicate and insignificant iterations so it will run a lot faster (and then it's still very slow). Then we display bottom line simulator results that are more meaningful in the Real World at the same time. For example, we use a worst case -10% annual rate of return. This is similar to what would have happened if you bought the DJIA at the top in 1929, saw 89% of your money disappear at the beginning of 1933, and then realized 11% from 1933 to 1939. Also from 1/1/1926 to 12/29/1950, over two decades, the DJIA was only averaged ~2% annually. A recent example of a bad ten-year return was from 1/1/2000 to 12/31/2009 - when the DJIA averaged only 1.30%. Then from 3/1/2000 to 2/28/2009 the DJIA averaged -1.77%. So as you can see, losing money in the stock market every year for more than ten years, and/or getting returns less than inflation for 25 years, is a reasonable worst-case scenario. This is because it has happened before. So this is how our Monte Carlo simulations work. We feel this is a much better methodology than other vendors that iterate from -50% to +50%, using historic standard deviations, long-term asset class averages, and other unrealistic scenarios that will have an extremely low probability of happening. How Our Monte Carlo Simulators Work Our range of returns are iterated from -5% to +9%. They are non-linear, and so there are more iterations closer to 9% than there are at -5%. Then there's more centered around 3%. So it is not a normally-distributed bell curve, like other vendors (nothing in money has a normal distribution curve in the Real World - so if you see one in money, then you know the creator is clueless). Then these are all repeated using two other combinations of realistic worst-case average tax (25%) and inflation rates (6%). So for every rate of return iteration, there are six variations of tax and inflation rates. This is how to correctly perform stress-testing on money. Now our Monte Carlo numbers reflect reality much more than any other vendor. All other vendors� numbers are still much too high � way past �rosy pie in the sky fantasy� - and have little-to-no chance of actually occurring in the Real World. Thinking these corporate shenanigans just to sell more money software (e.g., MGP) has anything to do with reality is a major life fail, so just wake up and don�t do that anymore. Our numbers are "right" and their numbers are "wrong" - just get over it and move on. Below are some screen prints for those that don't think it's possible for things to be screwed up so badly, and thus averaging somewhere between -5% to 5% long-term on a diversified investment portfolio is not realistic (right click and Save Target As... to download them, so you can see the details). This first screen print shows the average return on the S&P 500. The long-term (11 years) average return of the S&P 500 was --1.48%.

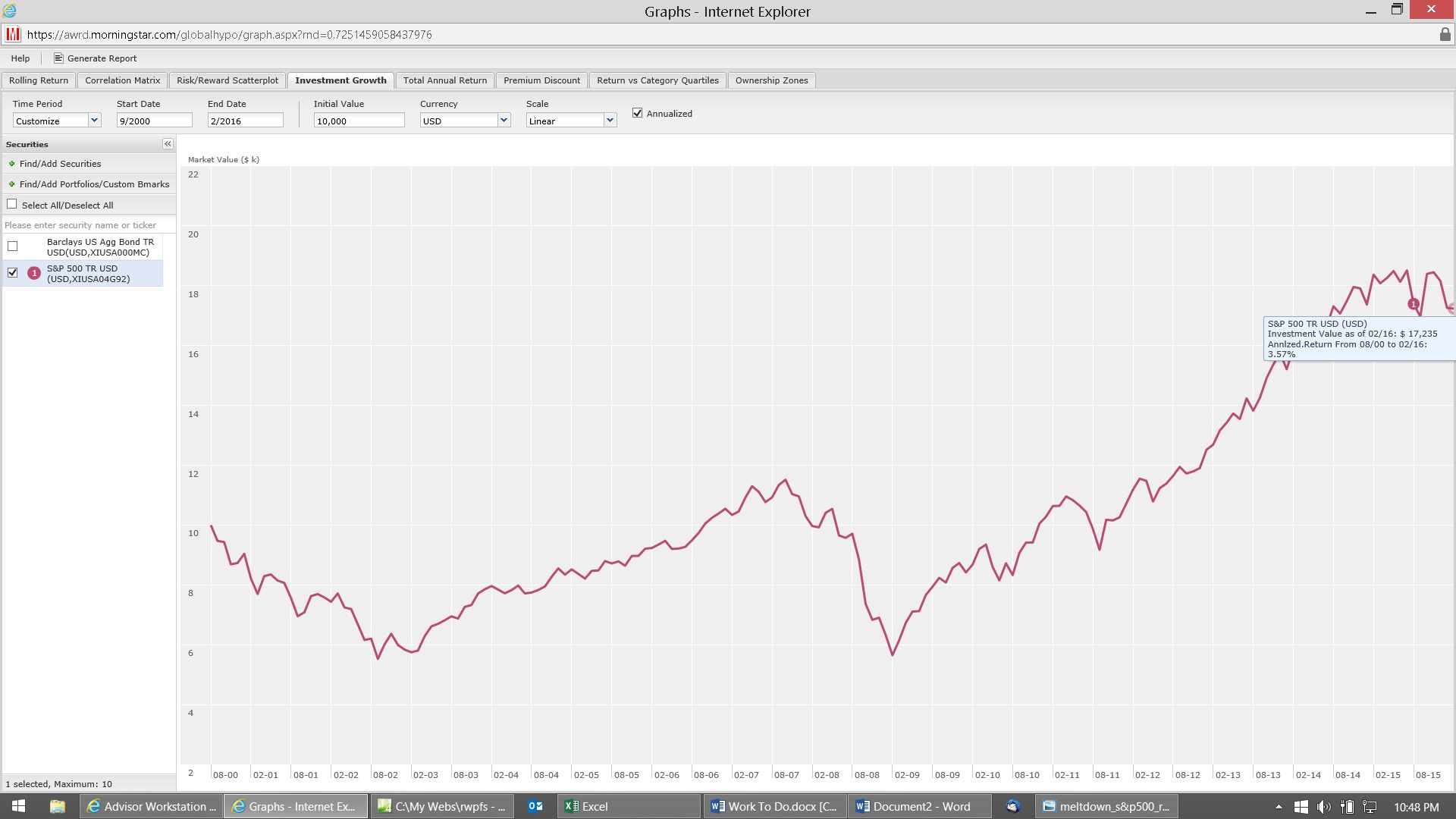

The screen print below shows the longer-term returns. Long-term stock market returns over 16 years: 3.57% (the return on bonds was 5.26%).

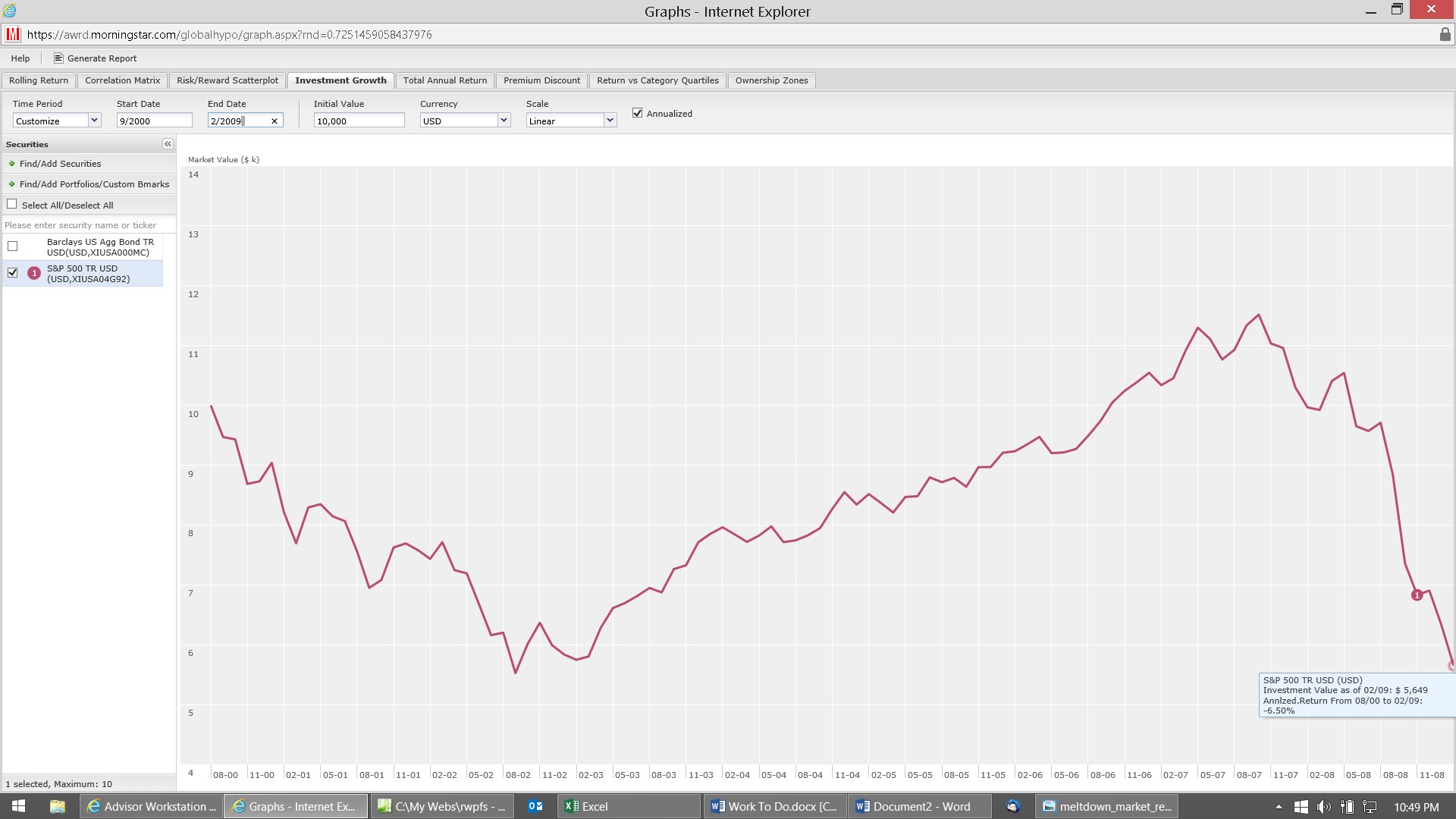

This screen print below shows the worst-case long-term (almost ten years) returns. You would have averaged a loss of 6.50% every year for almost ten years if you would have invested in the S&P 500 on 1 Sept 2000, and then sold after everything financial melted down in January 2009:

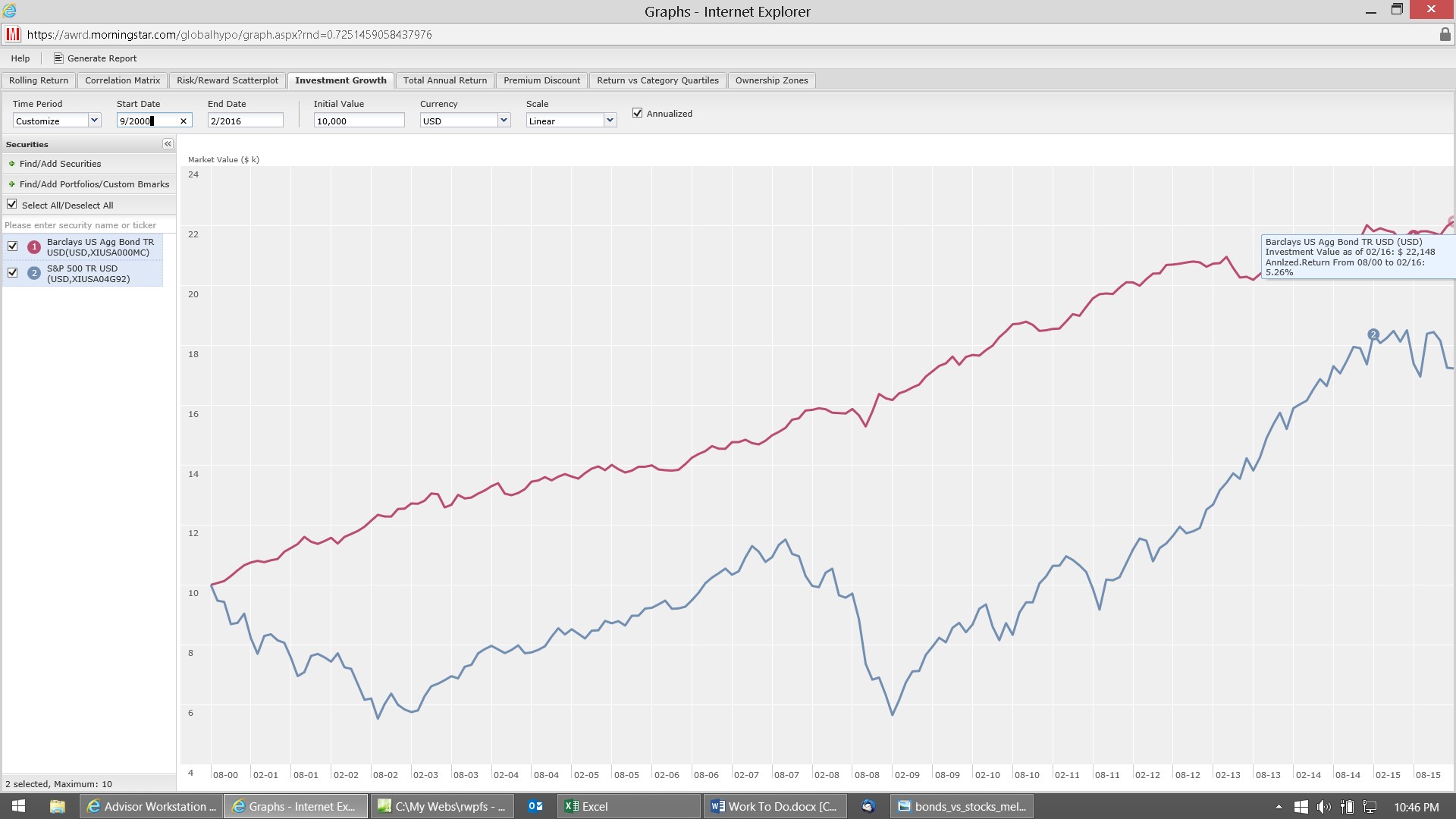

The next image shows the long-term returns of stocks and bonds. As you can see, bonds can outperform stocks.

So as you can see, not only can these debacles occur, they do - pretty much every decade. So count on more... much more. This is why our probability numbers are so low. No other money software vendor has a clue about what has happened in the past, what's going on now, nor what's coming; so their simulators are still using rosy scenario pie in the sky wishful thinking rate of return numbers from the last century. This is a typical money software problem where the programmers are clueless about money, and just take orders from management about how to program such things - which are also usually clueless about how money actually works in the Real World. This is why if you care about this, then much more analysis into the vendor's methodology is required than you thought. So if you want to get a grip on how your money may do long-term in the future, then another bottom line is that you cannot trust numbers from software vendors that don't care about reality, and only care about sales (MGP). So don't get all excited about Monte Carlo programs being added to personal investment software - it's mostly still just marketing at this point. This is great stuff for corporate finance people, or stock or derivative analysts, because they need it and will pay software vendors the big bucks to produce real Monte Carlo software. But this is not so when it comes to personal financial planning software for living investors; yet anyway. Here's why our financial plan software, even without using the Monte Carlo simulator does better than even the most expensive retirement software with it: You can change what you think the investment account's rate of returns will be in every year - all individually, before and after retirement. So you can model any kind of market environment you want, solve the tree-trunk problem by just inputting back-to-back years of negative returns, and have total control over all of the other details of someone's financial life at the same time. In addition to that, it has a more realistic Monte Carlo simulation capability than any other financial software vendor. Then you can compare these two methods, by manually inputting what you think a worst-case scenario is into the Current version, and then input an average forecast into the Proposed version (and then run the simulator function on that). That's something you cannot do with any other vendor's retirement plan software. Then by using Excel's built-in Goal Seek function, you can also easily solve for most any What-if you can think of - like determining the minimum rate of return needed on all investments, and/or just one investment account at a time, to reach the retirement goal. These built-in features are even more valuable than the Monte Carlo simulation results. Conclusions The reason Monte Carlo simulators are mostly useless, is because none of these programs account for all of the important details of someone's Real World situation. Then no retirement planning software vendor uses anywhere near the correct programming methodologies needed to even get into reality's ballpark (not even ours). All current Monte Carlo simulators only function in a one-dimensional environment, when financial and retirement planning is multi-dimensional. Because it takes so much calculating power, everything is stripped down (AKA dumbed down) just to display this mostly useless probability number, as quickly as possible. What's useful (in retirement planning) is estimating how well off you'll be in terms of comparing how much money you'll want to spend with how much money you can get, and/or how long it will last, compared to how long one expects to live. What users want to see are worst case scenarios that are likely to happen. In the Real World, the optimal way of simulating that, is just to input low investment returns, with high inflation and tax rates. This way, you'll know what the results could be given those exact worst-case assumptions. Forecasting what may most likely happen with these factors over time (given the assumed fluctuations in the markets - which you can control every year by using different rates of return on every investment for every year - including negative rates of return, and being able to change your income goal every year) is much more important to model, than a one-dimensional probability number, to an actual investor's life. So don't be taken in by Monte Carlo because some big-shot financial guru (e.g., William Sharpe) is touting it (by spending small fortunes on advertising). They're just trying to get advisors and investors to buy more of their software, because this is how they make their money. So even though it's interesting, and has promise someday, it's still much too primitive to be "Real World;" and is virtually useless in today's financial planning and investment management businesses. Even ours is semi-useless, but it's what customers want, and "they're always right," so that's want we gave them! |

Financial Planning Software Modules For Sale (are listed below) Financial Planning Software that's Fully-Integrated Goals-Only "Financial Planning Software" Retirement Planning Software Menu: Something for Everyone Comprehensive Asset Allocation Software Model Portfolio Allocations with Historical Returns Monthly-updated ETF and Mutual Fund Picks DIY Investment Portfolio Benchmarking Program Financial Planning Fact Finders for Financial Planners Gathering Data from Clients Investment Policy Statement Software (IPS) Life Insurance Calculator (AKA Capital Needs Analysis Software) Bond Calculators for Duration, Convexity, YTM, Accretion, and Amortization Investment Software for Comparing the 27 Most Popular Methods of Investing Rental Real Estate Investing Software Net Worth Calculator (Balance Sheet Maker) and 75-year Net Worth Projector Financial Seminar Covering Retirement Planning and Investment Management Sales Tools for Financial Adviser Marketing Personal Budget Software and 75-year Cash Flow Projector TVM Financial Tools and Financial Calculators Our Unique Financial Services Buy or Sell a Financial Planning Practice Miscellaneous Pages of Interest Primer Tutorial to Learn the Basics of Financial Planning Software About the Department of Labor's New Fiduciary Rules Using Asset Allocation to Manage Money Download Brokerage Data into Spreadsheets How to Integrate Financial Planning Software Modules to Share Data CRM and Portfolio Management Software About Efficient Frontier Portfolio Optimizers Calculating Your Investment Risk Tolerance |

© Copyright 1997 - 2018 Tools For Money, All Rights Reserved