Instructions for the Goals-Only Financial Planning Software |

| Download the Single Goals-Only Planner Demo | Download the Goals-Only Financial Planner Demo (coming soon) | Go to the Main Goals-Only Financial Planner Product Page |

| Site Information (is listed below. The financial planning software modules for sale are on the right-side column) Confused? It Makes More Sense if You Start at the Home Page How to Buy Investment Software Financial Planning Software Support Financial Planner Software Updates Site Information, Ordering Security, Privacy, FAQs Questions about Personal Finance Software? Call (707) 996-9664 or Send E-mail to support@toolsformoney.com Free Downloads and Money Tools Free Sample Comprehensive Financial Plans Free Money Software Downloads, Tutorials, Primers, Freebies, Investing Tips, and Other Resources List of Free Financial Planning Software Demos Selected Links to Other Relevant Money Websites

|

First, here are some generic directions that apply to most of the personal finance software on this site:

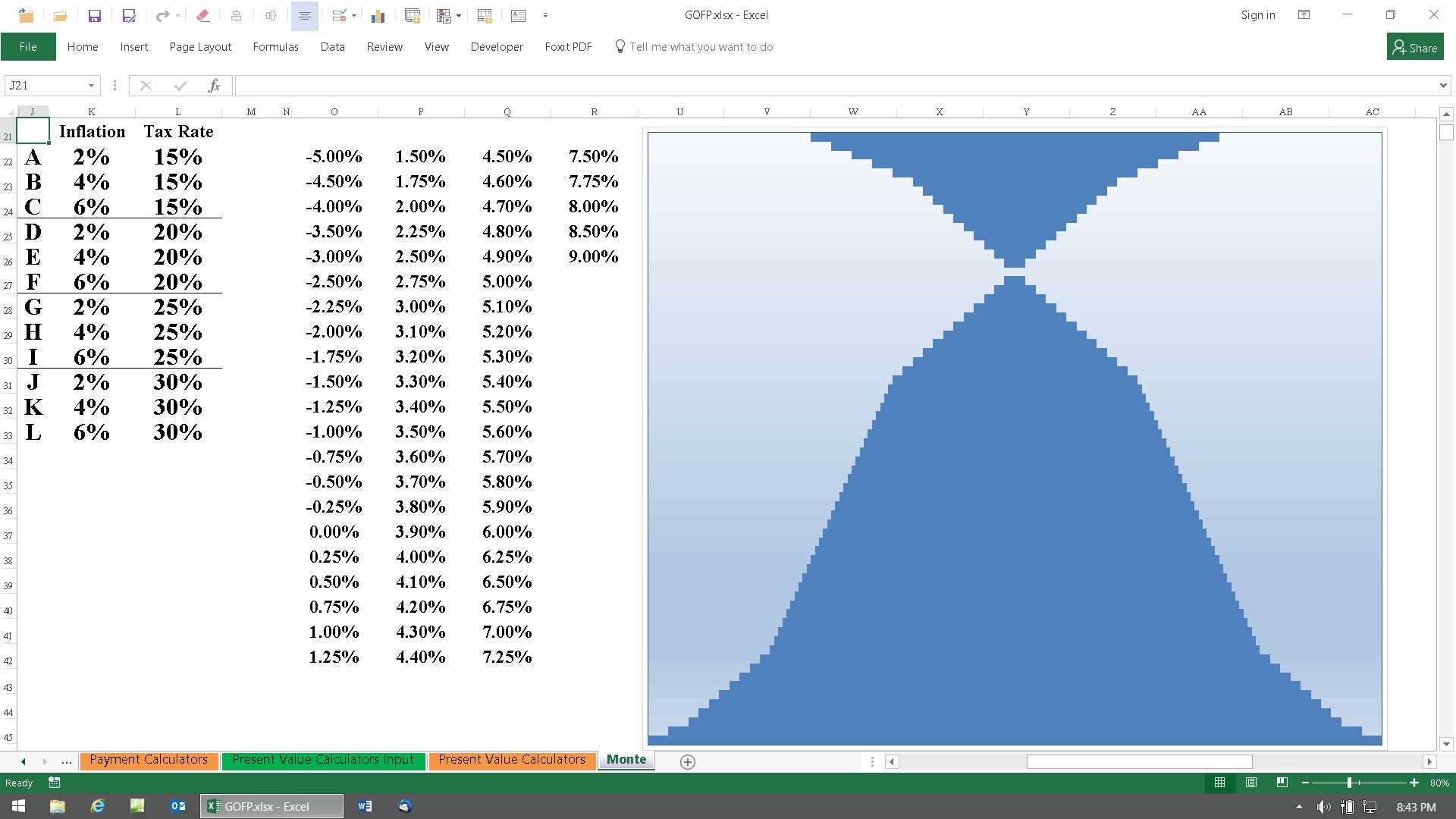

If you're still shopping, or making your first report, the best results are obtained by looking at the Goals-Only Financial Software demo, while following along as you read these directions. When you're using the program, things go better if you first print out these directions. Click "Enable Editing" to make it so you can change inputs. If you don't do this, then "nothing will happen" when you input data. Any change is editing (according to MS). This occurs because the program is not in a "Trusted Location." Go to File, Options, Trust Center, to fix that. The "demo" is the actual financial spreadsheet without the formulas, so you won't be able to do anything but look at it. You'll receive a working program after purchase. If you try to print the demo directly from your browser, or you just click Print in Excel, it probably won't work well. Tips for working with and printing in Excel are here, here, and here. If you need to print something on a password protected sheet, and you need to tinker with column and row sizes, and you bought support, and it's in Excel 2007 format, then you can get a version sent to you that does that. You switch between the sheets (pages) that make up the workbook (AKA spreadsheet) by either clicking on the sheet tab names at the bottom left of the Excel window, or by pressing Control Page Up or Down (pressing the Control key and either the Page Up or Page Down key at the same time). How to turn a zipped file attached in your e-mail (if any) into an Excel spreadsheet is explained in the text of the delivery e-mail. If you're seeing this: ####, then either change your Zoom magnification number (using the slider at the bottom right), or make the column width wider. If you see this: #REF! after completing your input, please respond to get a new program immediately. This usually means data was lost either via e-mail, unzipping, or while making a CD. If a red Error! dialog box comes up saying your input must be confined to a range of values, and your input was within that range, then the problem is that the input cell doesn't accept pennies. Try again rounding the value to the nearest dollar. If it still happens, then send e-mail with the spreadsheet name, sheet tab name, and exact cell number, so it can be changed. Before getting started, save an unused copy of all of the files in a separate folder, so you'll always have the original unaltered files somewhere. Then if you do something like delete a formula, you can easily fix it by copying it back using these original files. Then save files you've worked on using a different file name (and into a different folder). Tips for advisers saving and organizing client files are here. Programs usually come without sample input data, but be sure to delete all of the sample / client input (everything in green-shaded cells) before inputting your data. About the colored cells: Medium or light gray is either a title heading, or an input cell after a non-zero value is input into it (it's green when either zero or empty). Peach (or pinkish, depending on your Excel version) is a (usually password protected) field that changes when input changes. Light gray cells are information-providing, non-input, cells that don't change with input. White cells usually don't have anything in them, except on the unprotected presentation sheets (and change when input changes). Anything red is usually bad (input error). About the colored sheet tabs: Blue is a presentation sheet. Light green is an input sheet. Green is both an input sheet, and a presentation sheet. Orange is a calculation sheet. Purple is something else. You should make CD (or at least USB flash drive) backups of all of your work at least on a monthly basis, and store the CD in a safe location, but not where your computer is. More generic free PC tips are here. You can copy the input areas to the unprotected Scratch Pad sheet, then make notes there, so you'll know why you did what you did in the future. If you're an investing consumer (not a professional financial planner working with clients), then when you read "client, prospect, or they," just think "you." You would be both the advisor and the client (or spouse). This is a very large spreadsheet, so it may take a few seconds to calculate. Look for the word "Calculate" at the bottom left and wait for it to go away before inputting more data. About financial planning software support. About getting custodian brokerage account data to download into spreadsheets. About financial plan software updates. About financial planning software integration (sharing data between modules) How to send financial plans to clients via e-mail, without sending the whole program. The Small Single Goal-Only Planner's Directions (SGOP) Step 1: Open Single GOFP.xlsm with MS Excel, after running Windows Update until there are no more updates. The Monte Carlo simulator macro will fail if your computer is not updated. Go to the Input sheet. Don't do anything with any sheet to the right of the Calculations sheet as that will break the updater macro. Also, there are no inputs on the Calculations sheet. Inputting anything into non-protected cells there will also break the updater, so just don't do that. Input the name of the goal into cell D2. Or not, all this does is make this text appear on the other pages. Leaving it blank will not effect any calculations. Step 2: Use the sliders from left to right to input data. Results show in both the Calculations and Presentation sheets. It's normal to get weird results until all data needed to perform the Time Value of Money calculations are input. If there is only a single goal with a future value, like buying something in the future, then set the End of Goal Age to be the same as the Withdrawal Start Age. Step 3: Check for input errors on the other two sheets and to see if what you input is in the ballpark of what you want and expected. Click the Update button to run the macro. This runs the Monte Carlo simulation and calculates the first three results in the middle table on the Presentation sheet. It will take several seconds, and it's normal for your "screen to jump around." There's no way to stop it other than going to Task Manager and ending Excel, so just wait. Note that state taxes are not changed in the Monte Carlo simulation. So if you want to stress test that, make that input be a bit higher before clicking the Update button. Step 3: Evaluate, format, and present the results on the Presentation sheet. That's all there is to it. After any input is changed, the first three sets of results that display in the middle table of the Presentation sheet will be wrong, along with the Probability of Success number, and those cells will be colored red with text that says you've changed an input, along with text in row 7 of the Calculations sheet. So you'll need to Update again after changing any input slider to update these four results. The results of the Monte Carlo simulation ends up in cell K14 of the Input sheet. This changes the bar chart, the icon in cell C18, the big text in row 18, and both the number and the color of cell J12. Because there's no password needed to unprotect the Presentation sheet, if you know what you're doing enough in Excel, you can change what numbers that make the icon change, what the big text says and its ranges, and the color of J12. Most all calculations transparently display every number in every year on the Calculations sheet. This way, you can input the same data into other goals-whatever planner you may also be using, to perform an audit to see which numbers are more accurate. Please report everything you find strange, wrong, interesting, whatever. If you're comparing, please paste screen shots of the inputs and results from the other program into a Word docx and send that too. If you think the Probability of Success number is way too low, it's not. You're just used to seeing bogus results of bogus Monte Carlo simulators from other goalware vendors. How and why everyone needs to "just get over it," are here. If you find it "too limited," then you're using the wrong program. This just does what it does and no more. For retirement planning, use one of the Real World Retirement planners here. For college planning, use one of the real college planners here. This is new, so there's a wide array of "unusual input" that will produce strange results. Send the file back with your input every time this happens so it can be "fixed." Directions for the Big Goals-Only Financial Planner Program (the GOFP) First, some overall methodology. There are twenty goals and two ways of calculating them (so ten each). Therefore, a way of making them all function in the most efficient way possible for all users needed to be invented. So here's how it works (the best way to see this is on the Funding & Prioritizations sheet of the demo): Primary Goals - there are eight in total, four are payment calculators and four are PV calculators. Secondary and Tertiary Goals - There are six in total, three are payment calculators and three are PV calculators. Payment calculators (PMT) are for calculating goals that have more than one annual payment - like retirement or college funding. Present value calculators (PV) are for calculating financial goals that only have one future lump sum payment - like buying a car. Note that if you don't like the way this can get convoluted on the presentation pages, then you can edit or delete this text all you want to. Next, each goal works independently from all other goals. The one and only thing that is shared between all goals, is the age of the person input into Primary Goal #1. This means that nothing you do with one goal affects any other goal - which is the exact opposite of what occurs with actual financial planning software (where everything you do affects everything else). The only other mixing of goals is on the Snapshot of All Goals sheet that allows you to evaluate information in different ways. While on this topic, note that updating a goal has no effect on other goals. Which brings up the next questions, "Why can't you just click one thing and have all goals updated at once?" This may be added in the future, but (because there's no way to get a macro to know if there's input somewhere or not, and then do something or not), it would take a long time to run, and most of it would be calculating data on goals with no data input, so you'd be waiting ten minutes each time for mostly nothing. About using the sliders: This was done because users want things to be "easy to use." A point to remember about them, is that if it becomes a pain to get the number you want, then you can always right click on it, choose Format Control, and then manually change the Current Value to whatever you want. Just remember to click someone else when you're done, because it's still selected when you're done editing via the menus. The thing there, is that most have formulas to convert the limited functionality of the sliders into useful input. Look at where the slider results go, to see its translation formula. As you can see with the controls, you can change the way they work in many ways. Step 1: Open GOFP.xlsm with MS Excel, after running Windows Update until there are no more updates. The Monte Carlo simulator macro may fail if your computer is not updated. Go to the Funding & Prioritizations sheet. This is where you input how much money is available to invest for future financial goals, both lump sum and in monthly payments. This part of the program works on the basic Real World concept that there's only so much money to work with. So start with how much is available to invest in total now into cell B5. Then input how much in monthly investments can be afforded for goals into cell D5. Check for input errors and to see if what you input is in the ballpark of what you want and expected. Step 2: Allocate and prioritize fundings. The program works with three levels of financial goals: Primary, Secondary, and Tertiary. Primary goals are the most important, are things that you can't live without, and can be looked at as "needs." Secondary goals are less important, and can be looked at as "wants that you'd probably survive without." Tertiary goals are least important, and can be looked at as "wishes, luxuries, and/or things that won't need to survive.." You'll be tinkering with divvying investment savings between the three types of goals as you go, so don't make a fuss about getting it perfect now. The first step is to make a guesstimate of how you want to divvy investments between the three types. Do this by moving the first group of sliders for both lump sum and payments until you're in the ballpark. The next group of sliders below is for Primary Goals. Note the difference between the gray shading. The darker shade is for payment calculators and the lighter is for present value calculators. Then always keep in mind that when you move a funding slider, all of the funds in goals to the right will have their funding numbers changed too. Step 3: Activate and input goals. The main on / off switch for each of the twenty goals is the name input cell. When there is anything in it's name input cell, then the goal is turned on. When there is nothing in the naming input cell, everything to do with just that one goal is turned off. Start by inputting the usual priority primary goal, which is retirement for the main breadwinner, into Primary Goal #1, which is Payment Calculator #1. Note that only the first two payment calculators have inputs for Social Security. This is where you'd input retirement as a goal - by going to the Payment Calculators Input sheet and inputting the name for Primary Goal #1 into cell D4. Next, use the slider from B5 to B7 to input the age of the main client. Note that this is the only reference to age throughout the program, other than Primary Goal #2, which is retirement for a second person (usually a spouse). Now note that each slider input that controls how much money is invested also has a manual override associated with it. This is because MS has a lot to work to do on their sliders. There's not many people using them in Excel, so they made them, then noticed that there was little-to-no demand, so they stopped working on them. So there's a list of mundane limitations. First, it's hard to get them to give you the exact number you want. Then you may notice that they're upside down - when you click the bottom scroll, it goes up instead of down. There is a rotational control, but it's dimmed, which means it's a future function MS hasn't gotten around to making work yet. Note that this is where you'd integrate downloaded data from custodians. Just open the file that has updated spreadsheet data, and then go to that cell in the GOFP, press "=" then click on the cell in the download with that fresh data, and press enter. Now whenever you get a fresh download, your goal calculations will be updated. This is essentially all other vendors, like MoneyGuidePro, are doing here. So get the slider as close as possible, and then input the exact numbers you want to use for both lump sum and monthly investments into the manual overrides below the slider. Manual overrides may be added to goal values if enough users ask for it. It's not there now because you can fudge the future value of goals. This is because most financial goals are in the future, and the chances of something costing exactly what you thought it would years beforehand are slim to none, and Slim left town. Now use all of the other sliders for Primary Goal #1 to get them into the ballpark. Once you've made a good first pass, click the Update button on the bottom right of each goal. This calculates the hard parts and runs the Monte Carlo simulation. It will take several seconds, and it's normal for your "screen to jump around." There's no way to stop it other than going to Task Manager and ending Excel, so just wait. Whenever you change an input, making the results of the hard calculations obsolete, red text will display letting you know this. Red shading will also display on the drill-down into the details sheets. So whenever this happens, just click the Update button again. Note that changing some input data does not make the update needed text appear. This is usually because you've changed the goal so much, like changing the dollar amount of the goal, that it's "new" and it would unusual that no other slider for that goal would be moved afterwards. Just remember that whenever you change input, you'll probably need to update. It's normal to get weird results until all data needed to perform the Time Value of Money calculations are input. If there is only a single goal with a future value, like buying something in the future, then set the End of Goal Age to be the same as the Withdrawal Start Age. Step 4: After inputting goals, then go back and redo your funding allocations. Then retinker with goal sliders. When dealing with funding, there are several things to note. First, the number below "of" is what's left. The percentage number below that is the percent of the total of one of the three goal sections and not just the amount for that goal. When you change a slider, it will change them all to the right in the same goal section. This is because goals to the right are funded with what remains after you've made your change. So when working, make your changes left to right. There's also a possible formatting problem on the far right goal slider. So if you get strange results, check to see if you need to move slider on contribution ages start to see a number show up, and not the text that days you have an age error. If you're not inputting contributions, then setting these ages won't do anything - unless it says "Age Error." Then just hold the bottom scroller until the number gets large enough to make that text turn into a number. Then always ensure that there's no money left over when dealing with the last (far right) goal input. Do this by holding both scrollers down for both lump sum and month contributions on the far right goal. You're good when both lump sum and monthly payments are $0 on the goal slider area to the right. That's all there is to it! Just input realistic data, and it should work fine. Please let us know whenever there's anything you don't understand, even if you didn't buy support. Calculating goals is easy, and there's not much to it. It's just two sets of ten simple TVM calculator that doesn't interact with each other. So if you don't get something, then it may need to be fixed, or presented better. Just e-mail it back to use with your input, and it will be fixed, and made better, if possible. Step 5: Printing and presenting. You're probably not going to use all twenty goals, so you'll want to hide the unused goal rows on the presentation sheets (as seen in the demo). A macro to automatically print everything is being considered. The problem here has always been formatting that will work on everyone's printer. Other things to note: - The state tax rate is unaffected (not iterated, but still accounted for) by the Monte Carlo simulator, which only tinkers with the Federal tax rate. - It's normal for your screen to jump around with partial content showing when the macro runs. - Don't skip inputting goals. For example, if you have two goals that are either PMT or PV, then input them in order of priority. In other words, if they're all secondary goals and PMT's, then input them into Secondary Goals #1 and then Secondary Goals #2 - not Secondary Goals #3. You don't have to, but it will keep things from becoming complex. - The workbook needs to be unprotected so the Monte Carlo macro can create scenario sheets. So don't delete sheets nor rename any of the existing sheet tabs, or it will break. Everything you ever wanted to know about Monte Carlo simulations and simulators, is here. Answer to the FAQ: Yes, the low numbers are correct. You're just not used to seeing numbers generated from planet Earth, because most all other goalware's probability numbers are straight from BizarroWorld. So bottom line, our numbers are correct for a human living on Earth in the 21st century, and all others numbers, especially MoneyGuidePro, are so high that their just fake. You're just going to have to over the fact that Wall Street corporations lie. - You can input directly into the calculation sheets, but this may goof up other things. - If there's no current lump sum input for a goal, and you want to use just monthly payments, then $1 will display automatically as the beginning value. - Remember that nothing on any presentation sheet is protected with a password, so you can change anything you want to - including all of the thresholds that make the icons, colors, and text change depending on the result of the Monte Carlo simulation. So if you want to make it say, "You're good to go!" when it's 50%, you can do that just by editing the formula. Then right clicking on the icon allows you to set the numbers that make it change (same with the colors too). Yes, that's all there is to it. The rest is just how you want to change the presentation sheets to display the information in ways that have meaning to you. So instead of doing it yourself, just let us know, and we'll probably do it for you for free. There's a bazillion ways to present goals, and we want them all to eventually be here. Working with financial goals is easy and financial planning work is hard! That's just the way it is. Disclaimer: Goalware is not financial planning software, so there's no way this program can know if you can really afford the amounts needed to invest. This image shows the input data used in the Monte Carlo simulator:

As you can see in the histogram (right click on it and Save As... to download it so you can see it better), the bigger the steps, the less iterations at those return rates. The rates at the top before it squeezes down to nothing are the negative rates of return. The space in the middle is the 0% rate of return. The more steps in less space, the less distance between the iterations. In other words, everything is centered and weighted around getting an average of ~5%. If you think this is low, then look at the Benchmark Index returns on the table on the main Asset Allocation page, and you'll see that most all long-term equity returns three years and over, are centered are 5.5%. Also note that bonds have mostly outperformed stocks since 2000. In other words, there's more iterations in the range that will probably actually occur these days, and less in the outlying ranges. In case you didn't know, nobody in the history of ever has realized over 9% long-term on a diversified investment portfolio, so the iterations stop at 8.5%. MGP will go over 11%, which is just not possible anymore. Long-term returns on the stock market have not even been that high in the history of ever, then when you add fixed income and other diversifiers, the chances of getting anywhere near 10% for more than a couple years in a row these days are slim to none, and Slim left town. This is an example of other vendors using just one of dozens of fantasy returns, along with the usual sales deceptions, from BizarroWorld. Also, as you can read on the main Monte Carlo information page, it's possible to realize -5% long-term in this century. So how it works is that is uses the first line of inflation and tax rate data (row A) at -3.5%. Then the rate of return stays at -3.5% as the other eleven rows of returns are iterated up to 8.5%. Then that repeats at the next inflation rate, then again with the higher tax rate, etc. and so forth. |

Financial Planning Software Modules For Sale (are listed below) Financial Planning Software that's Fully-Integrated Goals-Only "Financial Planning Software" Retirement Planning Software Menu: Something for Everyone Comprehensive Asset Allocation Software Model Portfolio Allocations with Historical Returns Monthly-updated ETF and Mutual Fund Picks DIY Investment Portfolio Benchmarking Program Financial Planning Fact Finders for Financial Planners Gathering Data from Clients Investment Policy Statement Software (IPS) Life Insurance Calculator (AKA Capital Needs Analysis Software) Bond Calculators for Duration, Convexity, YTM, Accretion, and Amortization Investment Software for Comparing the 27 Most Popular Methods of Investing Rental Real Estate Investing Software Net Worth Calculator (Balance Sheet Maker) and 75-year Net Worth Projector Financial Seminar Covering Retirement Planning and Investment Management Sales Tools for Financial Adviser Marketing Personal Budget Software and 75-year Cash Flow Projector TVM Financial Tools and Financial Calculators Our Unique Financial Services Buy or Sell a Financial Planning Practice Miscellaneous Pages of Interest Primer Tutorial to Learn the Basics of Financial Planning Software About the Department of Labor's New Fiduciary Rules Using Asset Allocation to Manage Money Download Brokerage Data into Spreadsheets How to Integrate Financial Planning Software Modules to Share Data CRM and Portfolio Management Software About Efficient Frontier Portfolio Optimizers Calculating Your Investment Risk Tolerance |

© Copyright 1997 - 2018 Tools For Money, All Rights Reserved